"Just as Congress was poised to ban imports of Russian oil, President Biden got the jump on them with an executive order. Despite the delay, it was the right thing to do as a national expression of moral outrage over Russian military atrocities.

The White House repeatedly explained its two‐week inaction by suggesting that U.S. gasoline prices depend on how much oil we buy from this one minor source of imports.

In late February Reuters reported, “As the White House developed the sanctions package… [officials] were concerned about the possible impacts of a loss of Russian oil supply at a time of rising U.S. gasoline prices … I want to limit the pain the American people are feeling at the gas pump. This is critical to me,” Biden said.”

Similarly, in a recent conference Press Secretary Jen Psaki said, “We don’t have a strategic interest in reducing the global supply of energy and that would raise prices at the gas pump.” She added, “We are looking at options we could take right now to cut U.S. consumption of Russian energy, but we are very focused on minimizing the impact to families. If you reduce supply in the global marketplace, you are going to raise gas prices.”

The White House needs a lesson in basic energy economics. The global market for oil depends on the amount demanded and supplied, not where it comes from or where it goes. The global market for crude oil does not depend on whether the U.S. imports oil from Russia or Canada, nor does it depend on whether Russia sells that oil to the U.S. or China.

Cutting U.S. consumption of oil from one country is not even a reduction of global demand, much less a reduction of global supply. The U.S. only bought 1.3% of Russia’s crude oil exports in 2020 and the U.K. only 1.5%, according to Statista, while China bought 32.8%. For U.S. to unilaterally ban U.S. oil imports from Russia (even if joined by the U.K.) would not reduce the global supply at all unless Russia could not sell such small amounts to any other country.

Speculators promptly lost money betting on the incoherent Psaki‐Biden theory of oil prices. A March 8 headline, from CNBC, was “Crude oil jumps as much as 7% on U.S. ban of Russian imports was quickly followed the next day by “U.S. oil prices take sudden leg downward,” with the April futures price down from $130 to $108.

A U.S. ban on Russian oil would not even lower global oil demand unless the U.S. made no effort to replace that tiny amount of oil by simply importing from another country or by diverting U.S. oil exports to domestic use. If stopping U.S. imports of Russian oil reduced global demand, that would push oil prices down – not up.

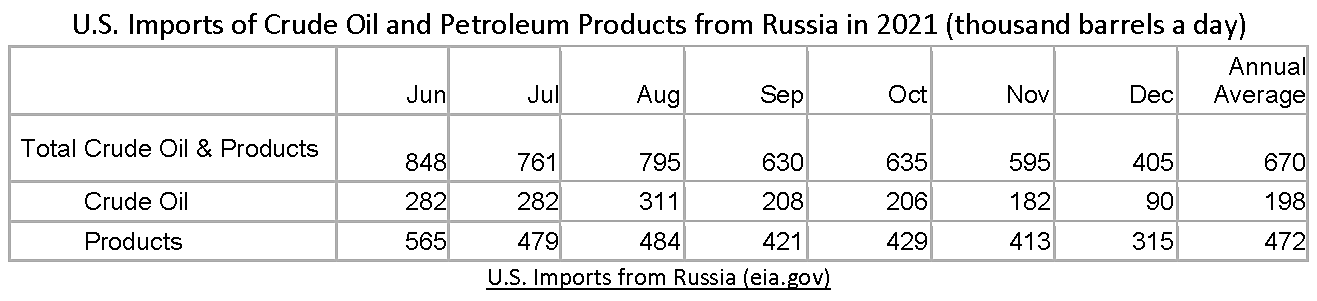

The Table shows that the U.S. imported 405,000 barrels per day (BPD) of oil and products last December but only 90,000 of that was crude oil. The annual average was 3% of U.S. crude oil imports, but that was cut by more than half by year end. Since December imports of Russian crude have slowed to a trickle of shipments leftover from past contracts, which must be phased out in 45 days. “Figuring that something like this might be coming, US companies have already started to prepare for the shift to other suppliers, domestic and foreign.”

Switching U.S. purchases from Russia to other suppliers does not change the size of global demand, only its location. Replacing Russian crude with oil from somewhere else would only reduce the global supply if Russia could not sell another 90,000 barrels a day to another country, such as China.

In 2021, more than 70% of what is usually counted as “Russian oil” imports in 2021 consisted of petroleum products “which include unfinished oils, such as naphtha, some types of fuel oil, and feedstock for refiners of heavy crude. Those products are used for further processing and are then used in refined goods exported largely to Mexico and South America.” Such semi‐refined products are not directly relevant to the world market and price for crude. And they can easily be replaced with domestic products, albeit with higher shipping costs to the East Coast. The U.S. could easily slash imports of Russian petroleum products by simply trimming much larger $89.4 billion U.S. exports of petroleum products in 2021.

The U.S. is big net exporter of liquified natural gas (LNG) and a small net exporter of coal, so we also don’t need those from Russia. The only reason the U.S. both imports and exports coal and LNG is to save a little on transportation costs when shipping from a foreign source is closer or cheaper than from a domestic port (such as VA for coal, TX for gasoline, and LA for LNG).

Relative shipping costs also help explain why the U.S. both imports and exports petroleum and refined products. As The Wall Street Journal recently explained: “The Jones Act, passed a century ago, has effectively limited the size of vessels that are allowed to transport goods between U.S. ports. That has left oil buyers on the West Coast and East Coast effectively unable to get supplies shipped out of the Gulf Coast.” If the new ban on importing Russian coal, LNG or fuel oil has any discernable regional effect on those domestic prices, it would only be through slightly higher transportation costs to the coasts.

Formally ending the small and shrinking U.S. imports of Russian crude will not be noticeably harmful to the U.S. because that vanishing trickle of Russian crude can easily be replaced with oil from Canada, Mexico, Latin America, or the Middle East – just as we previously switched to importing more Russian oil after imposing sanctions on Iran and Venezuela (who now look like the lesser of three evils)."

Friday, March 11, 2022

The Unintelligible Psaki‐Biden Theory of Oil Prices

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.