By Scott Sumner & Patrick Horan.

"Modern Monetary Theory (or MMT) is a macroeconomic model that has become popular among some heterodox economists and progressive policymakers, and is often cited by those who favor expanding the size of government. To understand the MMT model, it helps to start with some basic accounting relationships for government finance. For instance, government spending is paid for with either taxes, debt, or money creation. MMT proponents argue that a government that issues its own currency will not default on its bonds because it has the power to issue as much money as needed to pay off the public debt. In their view, this gives governments the ability to fund expensive public projects such as universal healthcare and a universal jobs guarantee without concern for the cost of these programs.

According to MMT proponents, there is a risk that deficit spending could lead to higher inflation once the economy is pushing beyond full capacity. If inflation were to rise, MMT proponents advocate raising taxes to hold down inflation. Most MMT proponents, however, do not regard inflation as a current risk for the US economy.

Unfortunately, the MMT prescription of monetizing debt would likely lead to high deficits, high inflation, or both. It could even lead to hyperinflation and all its associated problems. Therefore, the Federal Reserve (Fed) is more likely to continue adhering to its mandate and refuse to monetize the debt. In that case, however, the burden of deficit spending would fall on future taxpayers, leading to slower economic growth. In addition, higher interest rates might discourage private investment.

How Conventional Fiscal Policy Works

Government spending can be paid for in one of three ways. The fiscal authorities can (1) raise revenue via taxes, (2) borrow money (by issuing government bonds) and engage in deficit spending, or (3) print money. The third option is often advocated by MMT proponents, whereas the first two are the more standard methods for governments (especially in developed countries) to finance their spending. Ultimately, all public spending must be financed with tax revenue, as the public debt must be serviced by future taxpayers, and even money creation imposes an “inflation tax” on the public.

Government spending involves an opportunity cost: the diversion of resources that could have been used by the private sector for either investment or consumption. When a government borrows, it diverts funds away from private sector borrowers, a process called “crowding out.” Furthermore, it must pay back its debt, including the principal and accrued interest. This imposes a burden on future taxpayers, especially if the interest rate rises over time. Some economists argue that the debt burden is currently not a problem, as the economy’s growth rate exceeds the interest rate on debt. However, this may no longer be true in the future, as increasing budget deficits put upward pressure on interest rates.

If the interest rate on government bonds exceeds the country’s growth rate, then even if taxes are sufficient to cover noninterest spending, the ratio of debt to GDP will continue to grow. If a government incurs sufficiently high debts, then creditworthiness may decline, pushing the interest rate on government debt still higher. Eventually, the debt ratio may become too high for the government to even service the debt, triggering a crisis. This is called a “sovereign debt trap,” which refers to a situation where the government can no longer pay back its debt and the only options are (1) to default on its debt obligations, (2) to print money, or (3) to acquire external gifts. Default is undesirable because the debtor government’s credit worthiness deteriorates further and financial markets could potentially destabilize. Printing money leads to higher and more unstable inflation, which is also undesirable as it creates uncertainty, distorts labor markets, and discourages saving and investment. Acquiring external gifts, even when possible, usually comes with stringent conditions.

Because all of these options are unattractive, prudent governments exercise some degree of fiscal restraint, not allowing the debt ratio to reach dangerous levels. While some deficit spending is manageable for a government with a good credit rating, excessive debt can be a drag on the economy, requiring sharp tax increases, inflationary money creation, or both.

The MMT Alternative

MMT proponents often suggest that governments do not need to pay for increased spending with higher taxes. Governments that use their own fiat currency can always issue more of that currency to pay back their debt. Thus, the government has no effective budget constraint, which means that budget deficits and accumulated debts are no longer problems in terms of imposing a burden on taxpayers. Extra government spending does not need to be “paid for.”

This does not mean that MMT rejects all principles of macroeconomics. As in traditional macro models, MMT acknowledges a limit to how much growth an economy can sustain, given available resources. When an economy is operating under this limit (called its “full potential”), then MMT proponents argue there is room for government to increase its deficits without raising inflation. Since an economy is viewed as being below its full potential if there are a substantial number of people who are involuntarily unemployed, MMT advocates frequently argue in favor of a government-provided jobs guarantee. Increased government spending only becomes problematic when the economy is above its sustainable full potential, which leads to increased inflation. If and when excessive inflation occurs, MMT calls for increasing taxes, reducing spending, or both.

Some MMT proponents advocate a policy of holding the interest rate on government bonds at zero indefinitely, which would eliminate the cost of servicing the public debt. At this point, government bonds would be an almost-perfect substitute for money. There is a tradeoff involved, however, as this policy also risks promoting high inflation, unless steep tax increases hold the budget deficit to very low levels.

Weaknesses of MMT

There are at least five major problems with MMT:

It has a flawed model of inflation, which overestimates the importance of economic slack.

It overestimates the revenue that can be earned from money creation.

It overestimates the potency of fiscal policy, while underestimating the effectiveness of monetary policy.

It overestimates the ability of fiscal authorities to control inflation.

It contains too few safeguards against the risks of excessive public debt.

MMT is partly based in a Phillips Curve model that was largely discredited by theoretical advances in the late 1960s. Prior to 1968, many economists saw a tradeoff between inflation and unemployment, which is represented by the famous “Phillips Curve.” This reflected the widespread view that inflation was caused by “overheating,” or economic output expanding beyond the economy’s potential. Inflation was only a problem (in this view) when unemployment fell to unsustainably low levels.

In 1967, Milton Friedman and Edmund Phelps showed that this theory was flawed and did not account for the role of expectations. Over the next few years, their “Natural Rate Hypothesis” was confirmed by events. Unemployment was relatively high during much of the period from 1972 to 1981, and yet the inflation rate averaged nearly 9 percent. In contrast, today the United States has only 4 percent unemployment, and yet inflation is slightly below 2 percent. Japan is at full employment, and has had virtually no inflation over the past quarter century.

In fact, the trend rate of inflation is determined by monetary policy, which can impact either the money supply (through open market operations) or money demand (through the payment of interest on bank reserves.) Short-term fluctuations in inflation are often correlated with changes in economic slack, but the underlying inflation process is caused by monetary policy, not economic overheating. Indeed, the unemployment rate will tend to return to its natural rate in the long run, regardless of any given trend rate of inflation. This is why, on average, countries with low inflation do not tend to have higher unemployment rates than countries with high inflation.

MMT proponents also overestimate the revenue that can be derived from money creation. They often talk about paying for new programs by printing money, but don’t seem to realize how little revenue can be earned in this way. Part of the confusion may result from recent innovations, such as “quantitative easing” (QE), which have given many pundits the impression that the government can create a lot of money without triggering inflation. But modern QE programs are nothing like the money-financed deficits that hard-pressed countries once relied upon to cover their bills.

Printing money is a source of revenue for the government if the new money does not earn interest. Thus, printing a $100 bill costs roughly 6 cents, yielding a profit of $99.94. This type of non- interest-bearing money is called “high-powered money,” which refers to the powerful effects resulting from the injection of more cash into the economy. When interest rates are positive, newly created non-interest-bearing currency is a sort of “hot potato,” which gets spent quickly, forcing up prices.

Until 2008, the entire monetary base (currency plus bank deposits at the Fed) was high-powered money. After 2008, however, the Fed began paying interest on bank deposits at the Fed, and thus most bank reserves are no longer high-powered money. QE programs that exchange interest-bearing reserves for interest-bearing government debt are very different from “printing money” in the classic sense, and do not provide a way of extinguishing public debt. The Fed’s purchase of Treasury bills reduces the government’s interest liabilities in one sense, but the new bank reserves are simply another form of government debt, which involve a roughly equal interest liability. It is true that the currency continues to pay no interest, and thus in theory the government could finance its activities by issuing new currency. But the amounts are far too small to make a meaningful difference. In the United States, the currency stock is just over 8 percent of GDP. If one assumes that nominal GDP rises at 4 percent a year on average and the currency ratio stays at roughly 8 percent of GDP, then revenue from money creation is only about 0.32 percent of GDP, a drop in the bucket compared to total federal spending, currently over 20 percent of GDP.

Of course, the government could eliminate interest on bank reserves and print almost unlimited amounts of base money, but this would result in high inflation. Even Keynesian economists such as Paul Krugman are skeptical of the MMT claim that printing money could finance a significant share of government spending without provoking hyperinflation:

When people expect inflation, they become reluctant to hold cash, which drive prices up and means that the government has to print more money to extract a given amount of real resources, which means higher inflation, etc. Do the math, and it becomes clear that any attempt to extract too much from seigniorage — more than a few percent of GDP, probably — leads to an infinite upward spiral in inflation. In effect, the currency is destroyed.

One academic study found that the maximum sustainable amount of inflation tax revenue is roughly 4 percent of GDP, which would generate an annual inflation rate of 266 percent!

The tendency for MMT proponents to overestimate the revenue potential of money creation is closely tied to a related error, underestimating the potency of monetary policy and overestimating the potency of fiscal policy. They err in arguing that fiscal policy is what ultimately determines inflation in places like the United States. Because inflation is currently low in the United States, MMT advocates have argued that there is room for government to increase its spending. However, inflation is low precisely because the Fed is not following MMT policy advice. It is monetary policy that determines inflation, not fiscal policy.

There is abundant empirical evidence in US history that points to the dominance of monetary policy. In 1968, President Lyndon Johnson raised taxes and balanced the budget to reduce high inflation. He was unsuccessful, and inflation continued to rise owing to expansionary monetary policy. Inflation only fell in the United States in the early 1980s, after the Fed under Paul Volcker reduced the growth of the money supply. Volcker’s actions occurred at the same time as rapidly rising US budget deficits under President Reagan. Since the 1990s, inflation in the United States has been consistently low despite widely varying fiscal policies, ranging from budget surpluses during 1999–2001 to high budget deficits today.

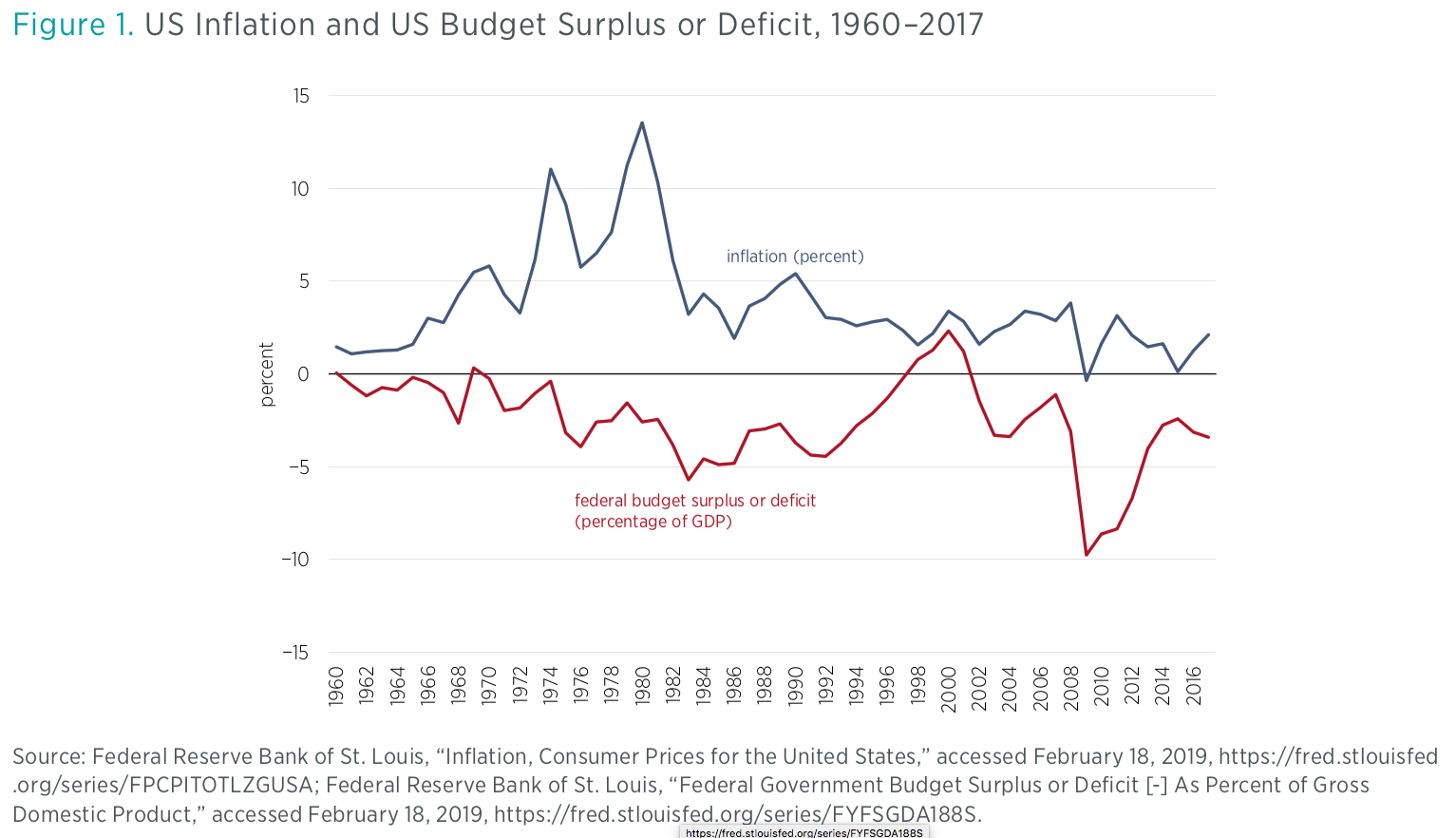

To illustrate this, figure 1 shows both the US budget deficit as a percentage of GDP and the inflation rate from 1960 to 2017. If MMT were correct, then one would expect to see increases in the deficit correlated with increases in inflation. However, despite dramatic increases in the budget deficit since 2001, inflation has not shown much variation.

Because MMT proponents overestimate the potency of fiscal policy, they mistakenly assume that fiscal policy can successfully control inflation. Today, central banks in most countries are independent and are charged with the task of stabilizing price levels. In most advanced countries, central banks are not required to support fiscal policy by lowering interest rates in order to allow governments to borrow more cheaply. Thus, monetary policy determines the path of inflation.

MMT’s explanation for inflation only works in places like Zimbabwe and Venezuela, where the central bank is subservient to fiscal policymakers, and thus central bank independence is eliminated. It is difficult to imagine why elected politicians, who adjust tax and spending policies in response to the interests of their constituents, would be more effective in controlling inflation than central bankers, who focus solely on that task.

If the MMT model is to be believed, then the roughly 2 percent inflation rate that has prevailed in the United States since 1991 owes to the deft actions of Congress in adjusting the budget deficit, not the decision of the Fed to try to keep inflation close to 2 percent. How likely does that seem? Congress has recently enacted tax and spending changes that have caused the budget deficit to soar, despite strong GDP growth and low unemployment. Does that seem like the action of an institution that can effectively target inflation at 2 percent?

Suppose that an MMT regime is implemented and inflation rises. The MMT prescription is to then raise taxes. Would Congress vote to increase taxes at a time when prices are already rising? Would the president also sign the legislation to increases taxes? It is difficult to imagine that the answer to these questions is yes, particularly with the current political gridlock in Washington, DC. Moreover, even if Congress possessed the political will to handle inflation responsibly, Congress would likely face serious informational challenges. Under the current regime, the Federal Open Market Committee (FOMC) meets roughly every six weeks to adjust its stance on monetary policy. If inflation were to become high, the FOMC would adjust monetary policy at its next scheduled meeting (or even call an emergency meeting if necessary). The Fed has decades of experience in learning how its policy tools affect the inflation rate. If inflation became a function of fiscal policy, Congress would have to learn how to adjust taxes in order to control inflation. This involves a learning curve that could prove very costly while inflation is doing serious damage to the economy. This is especially true if a zero-interest-rate policy were adopted, which would reduce the impact of tax changes on inflation.

Perhaps the most fundamental problem with proponents of MMT is their complacent attitude toward public debt and deficits. In fairness, this perspective is not without some justification and is shared by a number of mainstream economists. It’s true that the United States is less likely to default than Greece, owing to the fact that it controls its own currency. And it’s true that the interest rate on government debt has recently been lower than the growth rate of the economy. There are respectable models that suggest the government can safely increase the size of the debt when interest rates fall below economic growth rates. The basic idea is that economic growth will allow the government to service a growing debt over time.

Nonetheless, there are real risks in ignoring the government’s budget constraint. Debt that looks very manageable in one economic environment might suddenly look unsustainable in another, as Greece discovered during the Great Recession. The United States probably won’t default on its debt, but there are other unpleasant scenarios to consider. Suppose the public is opposed to extremely high inflation and Congress is thus unwilling to change the Fed’s low inflation mandate. In that case, a future budget crisis might lead to draconian tax increases, which stifle economic growth. Furthermore, even if the public were to tolerate high inflation, high inflation may only be able to fund a few years of government expenditures before a crisis occurs.

Even though economic growth currently exceeds the interest rate on public debt, this may not always be true. Consider how few economists during the 1980s would have anticipated near-zero interest rates in 2010. Also consider the projections that an aging population and growing healthcare costs will put increasing strains on the federal budget, pushing the debt-to-GDP ratio much higher during the 21st century. And then consider that Congressional Budget Office budget projections tend to assume continued economic growth, whereas the United States is likely to continue experiencing occasional recessions, which generally cause the deficit to get much larger. A responsible government does not incur debts that are only manageable if everything goes well. If history teaches us anything, it is to expect the unexpected.

Conclusion

MMT relies on dubious assertions about the causes of inflation and the respective roles of monetary and fiscal policy. It also rests on the unrealistic view that fiscal authorities would do an adequate job in managing inflation. An MMT agenda of having fiscal authorities manage monetary policy runs the risk of very high debts, inflation, or both—and both can be very harmful to the broader economy. Rather than rely on MMT, it would better for the Fed to ensure a stable, rules-based monetary policy, and for policymakers in Congress to exercise prudence in setting fiscal policy."

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.