"George Selgin has an excellent post on the history of FDIC. I already knew that FDR had opposed the idea of deposit insurance and was pressured into agreeing to the proposal in order to achieve his other banking reform goals. But this was new to me

Carter Golembe (1960, 195) zeros in on the truth. “[I]t is not reading too much into history,” Golembe says, to regard deposit insurance schemes as “attempts to maintain a banking system composed of thousands of independent banks by alleviating one serious shortcoming of such a system: its proneness to bank suspensions, in good times and bad.” Henry Steagall, who was second to none in his determination to save the United States’ small unit banks, made no bones about this. “This bill,” he said, referring to his May 1933 effort, “will preserve independent dual banking in the United States. … This is what the bill is intended to do” (ibid., 198).

Insurance and branching were, in short, rival reform options; one sought to preserve the unit banking status quo, and particularly state-chartered unit banks, despite their inherent weaknesses; the other would instead have allowed banks to branch statewide, if not nationwide, which would have meant more relatively large and well-diversified banks with branches, and many fewer smaller unit banks. Steagall favored the insurance option, while opposing branch banking tooth-and-nail. Carter Glass, his Senate Banking Committee counterpart, took the opposite position.

I increasingly believe that it makes sense to view federal deposit insurance and the small banking bias of our regulatory system as part of a unified regime that aims to create moral hazard—to encourage banks to take socially excessive risks. From the point of view of Congress, this risk-taking is a feature, not a bug. That’s why neither political party is proposing any sort of reforms to fix the problem. Indeed the problem is likely to get worse over time.

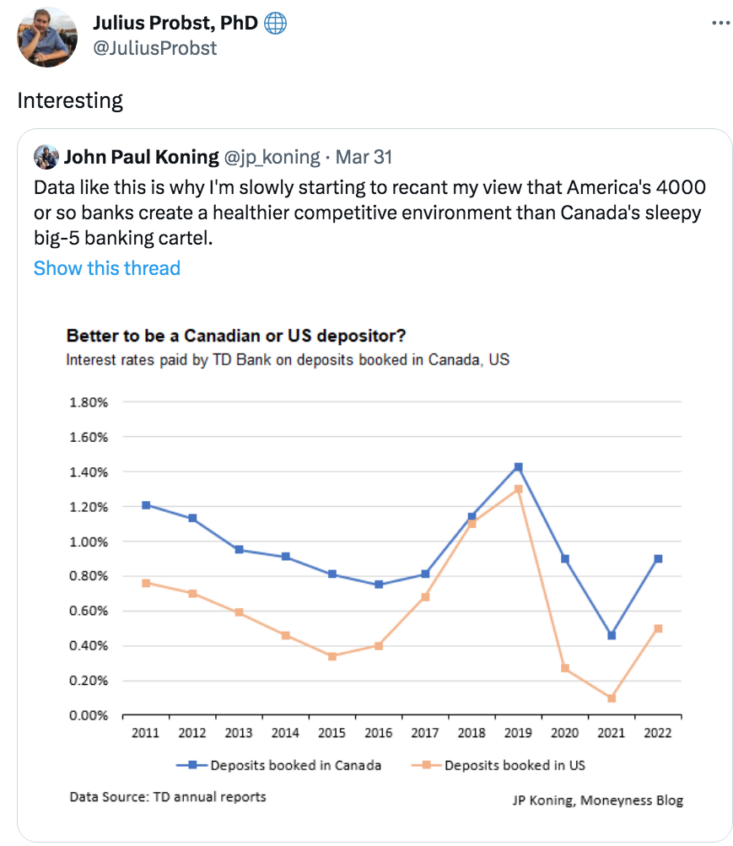

In a free market regime, the US system would consolidate into a smaller number of large, well diversified banks. Some worry that adoption of the Canadian approach would offer too little choice to consumers. But the US is much larger than Canada, and would end up with more than 5 large banks. In any case, this tweet casts doubt on the view that concentration hurts depositors:

Update: This post was certainly not well timed!"

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.