1. "In the late-1980s and early-1990s ACORN and other community groups claimed that Fannie and Freddie were standing in the way of their efforts to replace traditional underwriting with flexible underwriting. They lobbied Congress to force the Government Sponsored Enterprises (GSEs) to abandon their traditional underwriting standards. The goal was to force the GSEs to replace their conservative underwriting standards with flexible ones, knowing that this would spur the rest of the market to do the same.

2. These community groups were successful in convincing Congress to impose affordable housing (AH) mandates on Fannie and Freddie. This set in motion 14 years of ever looser loan standards.

3. Fannie embraced AH mandates in order to buy the political protection it would use to defeat any unwelcome changes to its lucrative charter benefits. To this purpose, it vows to “transform” the housing finance system. The strategy worked–Fannie was politically unassailable until 2008.

4. The government implements the National Homeownership Strategy with the goal of replacing traditional underwriting with flexible standards.

5. Dissenting voices (AEI's Peter Wallison among them) predicted that these efforts to transform housing finance would end in disaster.

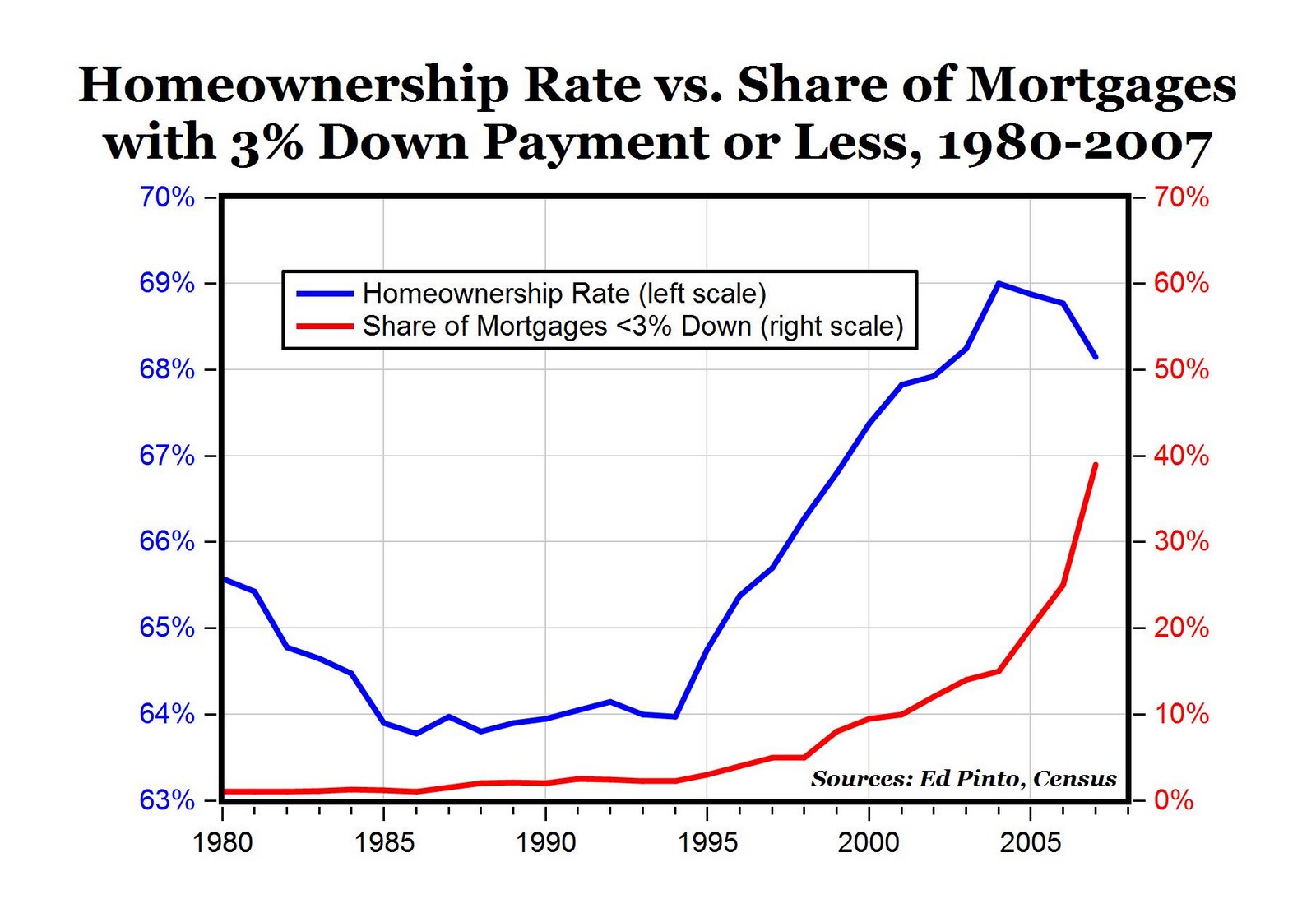

6. As flexible lending expands, the volume and risk characteristics of so-called prime loans increases markedly, yet these loans were still called prime. For example, loans with no downpayment acquired by Fannie are called prime merely because Fannie is now willing to acquire them. The same logic applies to loans with impaired credit. HUD acknowledges this in a 2000 rule making.

7. The United States, alone among developed countries, turned its prudential regulation of underwriting standards over to a social welfare agency, namely HUD. In 2004, HUD extols its “revolution in affordable lending.”

Conclusion: The major cause of the financial crisis in the United States was the collapse of housing and mortgage markets resulting from an accumulation of an unprecedented number of weak and risky Non-Traditional Mortgages (NTMs). These NTMs began to default en masse beginning in 2006, triggering the collapse of the worldwide market for mortgage-backed securities and in turn triggering the instability and insolvency of financial institutions that we call the financial crisis. Government policies forced a systematic industry-wide loosening of underwriting standards in an effort to promote affordable housing, compounded by moral hazard spread by Fannie and Freddie."

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.