Evaluating the free market by comparing it to the alternatives (We don't need more regulations, We don't need more price controls, No Socialism in the courtroom, Hey, White House, leave us all alone)

Wednesday, April 24, 2024

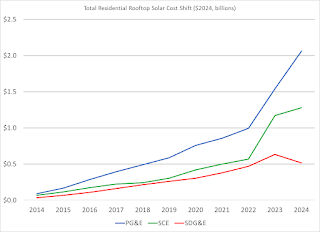

California’s Exploding Rooftop Solar Cost Shift

In 2024, residential PV will shift nearly $4 billion onto others’ bills, more than double the 2020 amount.

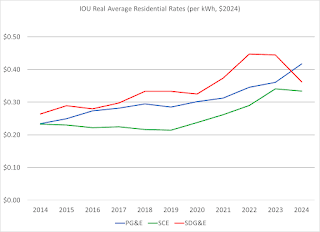

"There’s a lot of anger in California right now about rising electricity

prices. Since 2020, residential rates of the two largest investor-owned

utilities – PG&E and Southern California Edison – have risen,

respectively, by 38% and 40% after adjusting for inflation.

Inflation adjusted rates of San Diego Gas & Electric, the third

largest, have only risen 11% during that time, but SDG&E was already

the most expensive in 2020. The prices of all three are now more than

double the national average. (There are going to be a lot of numbers in this post. If you want the details behind them, this link has a data appendix with the data and code for my calculations.)

Regardless of what is driving utility costs higher, their impact on

rates is multiplied when customers install their own generation and buy

fewer kilowatts-hours from the grid. That’s because those households –

whether they are customers of the utility or of a community choice

aggregator – contribute less towards all of the fixed costs

in the system, such as vegetation management, grid hardening,

distribution line undergrounding, EV charging stations, subsidies for

low income customers, energy efficiency programs, and the poles and

wires that we all rely on whether we are taking electricity off the grid

or putting it onto the grid from our rooftop PV systems.

Since those fixed costs still need to be paid, rates go up, shifting costs onto the kWhs still being bought from the grid.

This will be less true for systems registered after last April when

compensation for new systems was made somewhat less generous, but that

applies to almost none of the systems installed before 2024, which are

the ones I am studying here.)

—

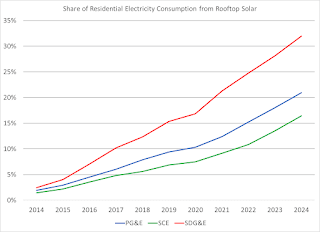

A decade ago, this was a small concern, because rooftop solar was

barely a blip in the total supply picture. In 2014, the homes served by

these three IOUs got less than 2% of their electricity off their roofs.

Today they get about 20%. As fewer kWhs are sold from the grid, retail

rates must rise even more in order to recover the fixed costs of the

system.

The problem has become particularly acute in the last four years.

During that time, solar capacity on houses has more than doubled at the

same time that the utilities’ fixed costs have escalated dramatically

due in large part to wildfires and the need for grid hardening against

them.

—

Figuring the rooftop solar cost shift

What has this done to rates? That takes a lot of calculations, which I

detail in the available data appendix. But it turns out that three

numbers are the major determinants: the total revenue the utility is

permitted to collect from residential customers to cover its operating

and fixed costs (known as the revenue requirement), the utility savings

from selling a customer fewer kWhs (known as the avoided cost), and the

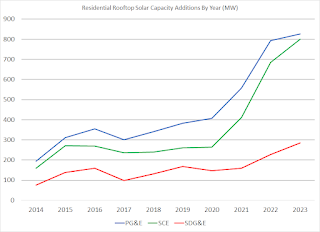

amount of solar on rooftops that is leading to those lower sales.

Since 2020, the real (i.e., inflation-adjusted) revenue requirements

of the utilities have increased about 25% for residential customers and

rooftop solar has grown 114%, but the avoided cost from each kWh coming

off those panels has hardly changed. So, as higher and higher

electricity prices have meant customers would save more and more for

each solar panel installed, the system hasn’t been saving any more money

per panel when they do, and those extra costs have been shifted onto

customers who don’t have solar.

—

Compared to the case in which residential rooftop solar were treated

like actual producers and paid the competitive value of their

generation, my analysis concludes that PG&E residential customers

with solar in 2024 will shift slightly more than $2 billion of costs to

customers paying the utility for their power. For Southern California

Edison, it’s around $1.3 billion, and for SDG&E the cost shift will

be about $0.5 billion. My findings are largely in line with a separate analysis

done by the independent Public Advocates Office of the CPUC. (Their

headline number – $6.5 billion for the total cost shift – differs

largely because they include commercial and industrial (C&I)

customers’ solar, which makes up about one-third of distributed solar

capacity, and because I use a somewhat more generous avoided cost than

their analysis does.)

The cost shift impact on rates

While it might be tempting to compare these astonishing figures to

the revenues collected from residential customers, that would implicitly

assume that all of these costs are shifted onto the residential price

of electricity. In reality, some costs are shifted onto C&I

customers. How much? That’s hard to know. It depends on which costs are

allocated to specific customer classes (e.g., the cost of distribution

lines in residential neighborhoods) and which are considered systemwide

costs (e.g., the cost of billing systems, transmission lines, etc.).

One thing we do know is that residential rates have increased faster

than C&I rates in the last decade. In 2014, PG&E residential

rates averaged about 7% above C&I, but by 2024, they were 15%

higher. SCE went from a 15% differential to a 47% differential over the

same time period, while SDG&E’s differential jumped from 2% to

19%. This suggests that the costs that have been going up lately, and

the increasing cost shift from distributed solar, have been allocated in

higher proportion to residential customers. That’s not surprising given

that a lot of the cost increases in the last few years have been

defensive investments to harden distribution systems – which are

disproportionately associated with residential customers – and because

homes have two-thirds of the distributed solar.

To get a feel for the impact, let’s assume that 60%-80% of the cost

shift from residential solar goes onto the bills of other residential

customers. If so, then 5.7-7.0 cents of the price of each kWh (for

customers not on the CARE low-income rate), or 12%-15% of PG&E’s

full residential price in 2024, is due to the rooftop solar cost shift.

For SCE it is 3.2-4.0 cents or 9%-11% of the price. And for SDG&E it

is 7.4-8.8 cents or 19%-22% of the price.

In 2018, Lucas Davis wrote a blog post titled “Why Am I Paying $65/year for Your Solar Panels?” The question is still with us today, except now it’s more like “Why Am I Paying $300/year for Your Solar Panels?”

Getting to a sustainable energy system

I’m not presenting this analysis in order to demonize solar adopters

or to make them feel guilty about their choice. It’s not their

responsibility to do this sort of analysis. People are busy and utility

bills are a burden for many. I don’t blame them for jumping at an

opportunity to save money, without working through where those savings

come from. The problem is not in our household decision makers, but in

our policies. The 2023 change in how new solar installations are

compensated was a small step in the right direction, but not a solution.

Nor is the solar cost shift the only problem facing California’s electricity system. Adapting to increased wildfire risk and other impacts of climate change, challenges of maintaining reliability with increased renewables, dysfunctional regulation, inefficient utility operations, and excessive returns on capital investments

are all contributing to increased rates. All of these issues –

including the exploding solar cost shift – need honest discussions among

legislators and policymakers if California is going to successfully

navigate today’s unsustainable rate trends."

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.