Evaluating the free market by comparing it to the alternatives (We don't need more regulations, We don't need more price controls, No Socialism in the courtroom, Hey, White House, leave us all alone)

"Politicians have recently called on the Federal Reserve to address

issues of racial and income inequality. Current and former Fed officials

have pointed out that monetary policy is too broad a tool to accomplish

this narrow goal. Yet the Fed may have the ability to affect inequality

by other, more effective means.

Presidential candidate Joe Biden has recommended

that “the Fed should aggressively enhance its surveillance and

targeting of persistent racial gaps in jobs, wages, and wealth.” A

similar proposal

by Senator Elizabeth Warren would require the Fed to pursue “the

elimination of disparities across racial and ethnic groups with respect

to employment, income, wealth, and access to affordable credit.”

Improving the livelihoods of minorities and low-income earners is a

noble goal. Economists widely agree, however, that these objectives

cannot be achieved using monetary policy.

Inequality is a long-term, structural issue that cannot be resolved

with monetary policy, as former Fed Chairs Ben Bernanke and Janet Yellen

have acknowledged. “The degree of inequality we see today,” Bernanke said,

“is primarily the result of deep structural changes in our economy that

have taken place over many years.” Because “monetary policy is a blunt

tool,” Bernanke argued that “policies designed to affect the

distribution of wealth and income are, appropriately, the province of

elected officials, not the Fed.”

In 2016 Congressional testimony, Yellen similarly emphasized the

broad nature of monetary policy. “A stronger labor market,” she said,

“will improve the status of all groups in the labor market.” But

addressing inequality is more difficult since “there are deeper

structural reasons that these trends continue.”

Current Fed Chair Jerome Powell also recently expressed skepticism

regarding the Fed’s ability to deal with income inequality. Noting the

broad nature of monetary policy, he said that “a tight labor market is

probably the best thing that the Fed can foster to go after that

problem.” Powell emphasized that Congress, rather than the Fed, may be

more equipped to deal with issues of inequality. “We don’t really have

tools that can address distributional disparate outcomes as well as

fiscal policy.”

The Fed does, however, have another means by which it can combat

inequality. It could eliminate excess regulations that inhibit bank

competition and the hiring of low-skilled workers.

Standard economics teaches that regulations tend to reduce

competition and economic efficiency. Until the 1990s, US banks were

generally prohibited from opening branches in other states and sometimes

even within their home state. These restrictions made the banking

industry less efficient, resulting in higher costs for bank customers. Restrictions on branch banking also make it difficult to diversify investments, which makes the banking system less stable.

From the 1970s through the 1990s, many states eliminated branch

banking restrictions, allowing greater competition in the banking

industry. Studies of this period find that eliminating these state-level

regulations lowered loan rates for borrowers, improved entrepreneurship, and reduced economic volatility.

In a 2010 study,

Thorsten Beck, Ross Levine, and Alexey Levkov consider whether

deregulations during this period affected income inequality. They look

at several measures of inequality such as the Gini coefficient, Theil

index, and the ratio of the 90th to 10th percentiles of income. The evidence shows that “branch deregulation substantially reduced income inequality.”

The authors are careful to account for other effects that might bias

their results. They control for local economic conditions, such as

state-level unemployment rates and GDP growth, demographic differences,

such as the percentages of blacks and female-headed households, and

other policies, such as labor market reforms. The results consistently

show that bank deregulation reduced inequality.

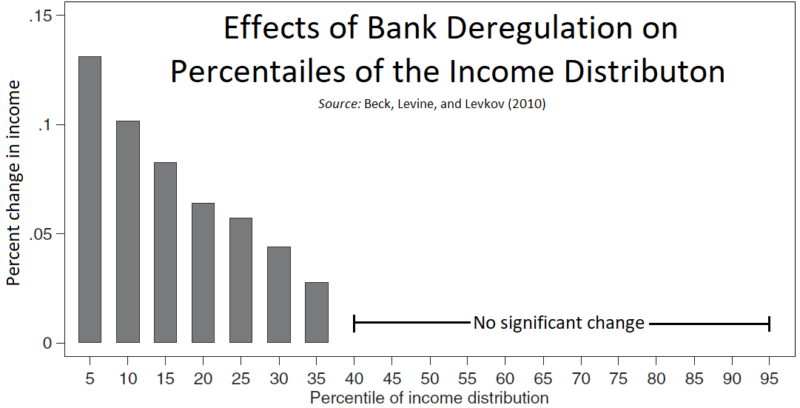

Beck, Levine, and Levkov also test whether reductions in inequality

are driven by changes at the low or high ends of the income

distribution. Their results, reproduced in the figure below, find that

deregulation was associated with gains to the lower levels of the income

distribution without significant effects on higher levels of the

distribution.

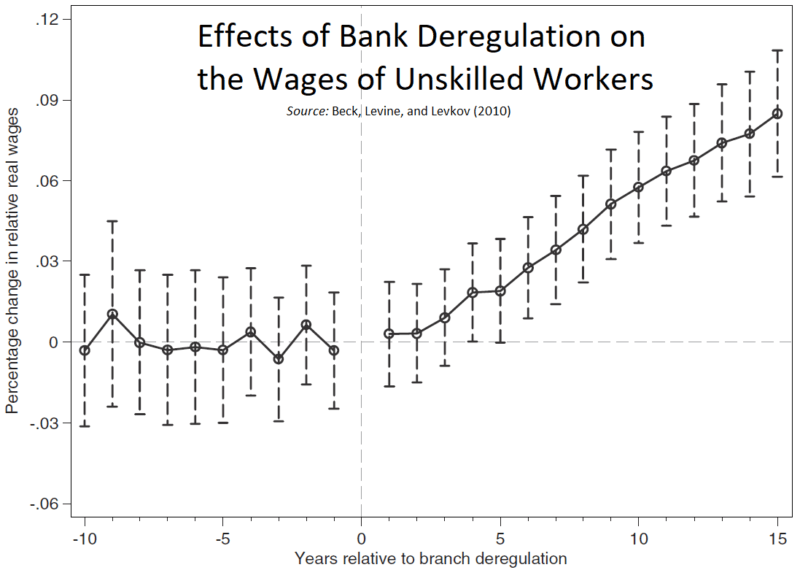

They further examine the timing of effects on workers at the lowest

income levels. As seen in the figure below, the relative real wages of

unskilled workers increased considerably in the years following

deregulation. Bank deregulation also appears to have boosted employment

opportunities as illustrated by lower rates of unemployment and higher

working hours for unskilled workers.

Bank deregulation since the 1970s has had important economic effects

of reducing income inequality and improving economic stability. The

evidence suggests that, unlike monetary policy, deregulation is one

avenue by which the Fed might have meaningful effects on reducing income

inequality.

To be clear: I am not recommending bank regulators relax their

emphasis on bank safety and soundness. Regulators must always remain

focused on financial stability, but trimming excess regulations would

reduce barriers to entry for new banks and ease the regulatory burdens

of smaller banks that pose no risk to the banking system. A study by Richard Herring, for instance, found that bank capital regulations “could be reduced by 75% with no loss of rigor.”

In fact, reducing the number of regulations can often be more

effective at constraining bank risk. In the same way that a complex tax

code creates loopholes to avoid the law, a complex regulatory system

enables banks to avoid compliance. Strong but simple regulations can improve financial stability without creating undue costs of regulatory compliance.

Nor am I suggesting that racial disparities be made a primary focus

of regulation. Efforts by the Consumer Financial Protection Bureau

(CFPB) to target discriminatory lending practices, for example, have

made lending to minorities more costly and less common.

A more prudent approach is to eliminate unnecessary barriers to

competition. Such a change is likely to increase opportunities for those

with lower incomes and narrow the wage gap between low-skilled and

high-skilled workers.

Economic theory suggests, and evidence confirms, that the burden of

regulations is likely to fall on the least well-off members of society.

Limiting regulation encourages competition in the banking system,

resulting in lower costs for consumers and more hiring of low-skilled

workers.

If the Fed aims to reduce inequality, it should use policies that are

known to be effective. There is little scope for affecting inequality

with monetary policy. Reducing banks’ regulatory burden reduces

inequality by improving the lives of Americans with the lowest incomes."

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.