"Based on the title of this column, you may think I’m going to write about oppressive IRS behavior or punitive tax policy.

Those are good guesses, but today’s “brutal tax beating” is about what happens when a left-leaning journalist writes a sophomoric column about tax policy and then gets corrected by an expert from the Tax Foundation.

The topic is the tax treatment of executive compensation, which is somewhat of a mess because part of Bill Clinton’s 1993 tax hike was a provision to bar companies from deducting executive compensation above $1 million when compiling their tax returns (which meant, for all intents and purposes, an additional back-door 35-percent tax penalty on salaries paid to CEO types). But to minimize the damaging impact of this discriminatory penalty, particularly on start-up firms, this extra tax didn’t apply to performance-based compensation such as stock options.

In a good and simple tax system, which taxes income only one time (including business income), the entire provision would be repealed.

But when Alvin Chang, a graphics reporter from Vox, wrote a column on this topic, he made the remarkable claim that somehow taxpayers are subsidizing big banks because the aforementioned penalty does not apply to performance-based compensation.

Since Mr. Chang is a graphics reporter, you won’t be surprised that he included several images to augment his argument.…the government doesn’t tax performance-based pay for…any…top bank executive in America. Unlike regular salaries — where the government takes out taxes to pay for Medicare, Social Security, and all other sorts of things — US tax code lets banks deduct the big bonuses they give to their executives. … The solution most Americans want is to either heavily tax CEO pay over a certain amount, or to set a strict cap on how much CEOs can make, relative to their workers. As long as this loophole is open, though, it makes sense for banks to continue paying executives these huge sums. ..for now, taxpayers are still ponying up to help make wealthy bankers even wealthier, because the US tax code encourages it.

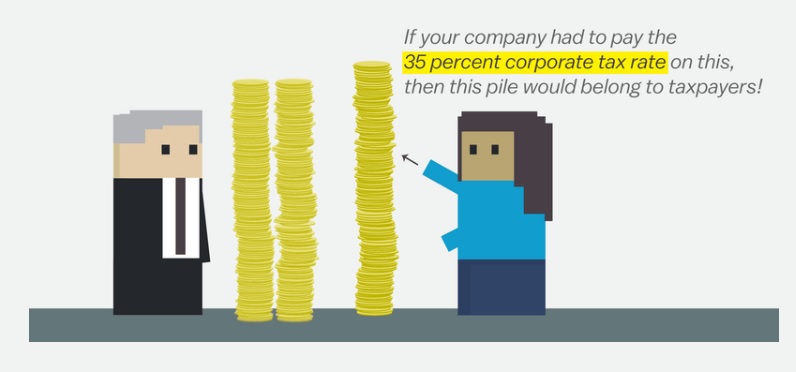

Here’s one making the case that companies should pay a 35 percent tax on performance-based pay for CEO types. Keep in mind, as you peruse this image, that recipients of performance-based pay have to declare that income on their 1040s and pay 39.6 percent individual income tax.

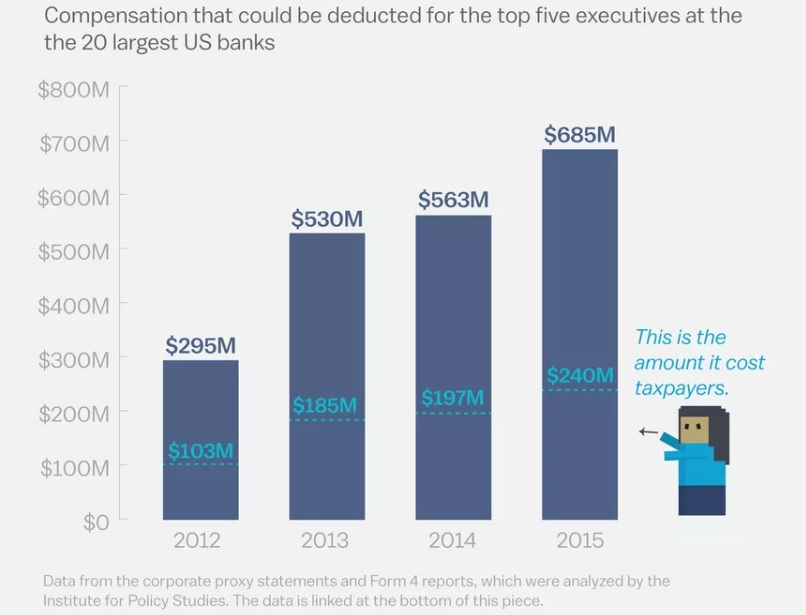

And here’s Chang’s look at how much money the IRS could have collected from big banks in recent years if the anti-CEO tax penalty was extended to performance-based pay.

When I look at these images, my gut reaction is to be offended that Chang equates “taxpayers” with the federal government.

So I would change the caption of the first image so it ended, “…this pile would be diverted from shareholders to politicians.”

And the caption in the second image would read, “This is the amount it saved taxpayers.”

But Chang’s argument is also flawed for much deeper reasons. Scott Greenberg of the Tax Foundation debunks his entire column. Not just debunks. Eviscerates. Destroys.

Here are some of the highlights.

…the article contains several factual errors and misleading claims about how CEOs are taxed in America. The article begins by making an incorrect claim: that the federal government does not tax performance-based CEO pay… This is simply untrue. Under the U.S. tax code, households are generally required to pay individual income taxes on the value of the stock options and bonuses that they receive…up to 39.6% on the performance-based pay… The article continues with another false assertion…it claims that CEO performance-based pay is not subject to the same Social Security and Medicare payroll taxes as “regular salaries.” In fact, all employee compensation, including CEO pay, is subject to Medicare payroll taxes, and high-income individuals actually pay a higher Medicare payroll tax rate than most other employees. …it claims that U.S. businesses are allowed to deduct CEO pay but are not allowed to deduct “regular salaries.” This is patently incorrect. Under the U.S. tax code, businesses are allowed to deduct virtually all compensation to employees. In fact, the only major exception to this rule is that businesses are only allowed to deduct $1 million in non-performance-based salaries to CEOs. This means that the U.S. tax code gives the same, if not worse, treatment to CEO compensation as “regular salaries.”Scott also addresses the silly assertion that deductions for CEO compensation are some sort of subsidy.

You probably wouldn’t claim that taxpayers are subsidizing the restaurant worker’s salary, because the deduction for employee compensation is a regular, structural feature of the tax code. In general, businesses in the U.S. are taxed on their revenues minus their expenses, and the salary paid to the worker is a business expense like any other. The same argument applies for CEO compensation. When a business pays a CEO $155 million, it has increased its expenses and decreased its profits. The normal logic of U.S. tax law dictates that the business be allowed to deduct the CEO’s compensation from its taxable income. Then, the CEO is required to pay individual income taxes on the compensation.The bottom line, as Scott points out, is that Bill Clinton’s provision means that CEO pay is penalized rather than subsidized.

…wages and salaries of CEOs are penalized relative to the wages and salaries of regular employees, while performance-based compensation is taxed in the same manner as regular wages and salaries. In sum, it is simply wrong to say that the federal tax code subsidizes CEO pay.Game, set, and match. Mr. Chang should stick to graphics rather than tax policy.

And policy makers should resist tax policies based on envy and resentment since the net result is a tax code that is needless complex and pointlessly destructive.

One final moral to the story: If there’s ever a tax fight between Vox and the Tax Foundation, always bet on the latter."

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.