"There’s a “convergence” theory in economics that suggests, over time, that “poor nations should catch up with rich nations.”

But in the real world, that seems to be the exception rather than the rule.

There’s an interesting and informative article at the St. Louis Federal Reserve Bank which explores this theory. It asks why most low-income and middle-income nations are not “converging” with countries from the developed world.

…only a few countries have been able to catch up with the high per capita income levels of the developed world and stay there. By American living standards (as representative of the developed world), most developing countries since 1960 have remained or been “trapped” at a constant low-income level relative to the U.S. This “low- or middle-income trap” phenomenon raises concern about the validity of the neoclassical growth theory, which predicts global economic convergence. Specifically, the Solow growth model suggests that income levels in poor economies will grow relatively faster than developed nations and eventually converge or catch up to these economies through capital accumulation… But, with just a few exceptions, that is not happening.Here’s a chart showing examples of nations that are – and aren’t – converging with the United States.

The authors analyze this data.

The figure above shows the rapid and persistent relative income growth (convergence) seen in Hong Kong, Singapore, Taiwan and Ireland beginning in the late 1960s all through the early 2000s to catch up or converge to the higher level of per capita income in the U.S. …In sharp contrast, per capita income relative to the U.S. remained constant and stagnant at 10 percent to 30 percent of U.S. income in the group of Latin American countries, which remained stuck in the middle-income trap and showed no sign of convergence to higher income levels… The lack of convergence is even more striking among low-income countries. Countries such as Bangladesh, El Salvador, Mozambique and Niger are stuck in a poverty trap, where their relative per capita income is constant and stagnant at or below 5 percent of the U.S. level.The article concludes by asking why some nations converge and others don’t.

Why do some countries remain stagnant in relative income levels while some others are able to continue growing faster than the frontier nations to achieve convergence? Is it caused by institutions, geographic locations or smart industrial policies?I’ll offer my answer to this question, though it doesn’t require any special insight.

Simply stated, Solow’s Growth Theory is correct, but needs to be augmented. Yes, nations should converge, but that won’t happen unless they have similar economic policies.

And if relatively poor nations want to converge in the right direction, that means they should liberalize their economies by shrinking government and reducing intervention.

Take a second look at the above chart above and ask whether there’s a commonality for the jurisdictions that are converging with the United States?

Why have Hong Kong, Singapore, Taiwan, and Ireland converged, while nations such as Mexico and Brazil remained flat?

The obvious answer is that the former group of jurisdictions have pursued, at least to some extent, pro-market policies.

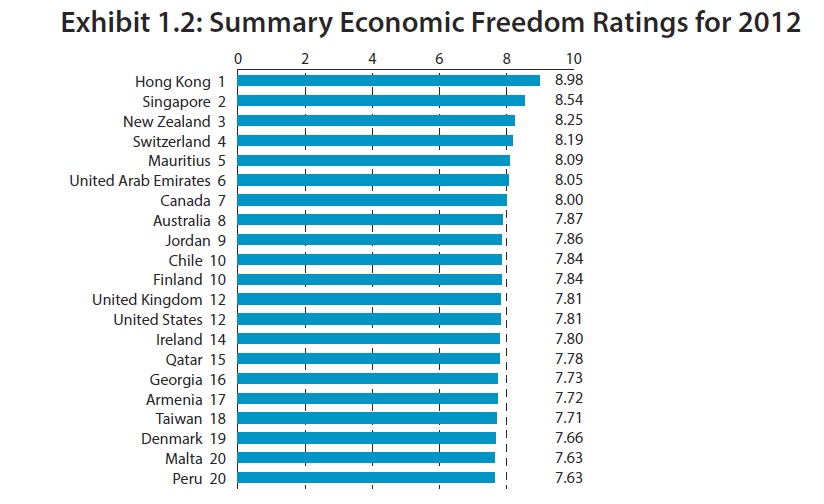

Heck, they all rank among the world’s top-18 nations for economic freedom.

Hong Kong and Singapore have been role models for economic liberty for several decades, so it’s no surprise that their living standards have enjoyed the most impressive increase.

But if you dig into the data, you’ll also see that Taiwan’s jump began when it boosted economic freedom beginning in the late 1970s. And Ireland’s golden years began when it increased economic freedom beginning in the late 1980s.

The moral of the story is – or at least should be – very clear: free markets and small government are the route to convergence."

Tuesday, March 31, 2015

Why have Hong Kong, Singapore, Taiwan, and Ireland converged, while nations such as Mexico and Brazil remained flat? The obvious answer is that the former group of jurisdictions have pursued, at least to some extent, pro-market policies.

By Daniel J. Mitchell of Cato.

The market is the best antidote to discrimination. It rewards talent and penalizes prejudice.

From Cafe Hayek.

"In today’s Wall Street Journal, Heather Mac Donald explains why it’s absurd to conclude that gender discrimination is genuinely practiced in competitive industries. (Gated)

For the record, I believe that every private employer has the moral right, and should have the legal right, to hire and fire whomever it wants for whatever reasons might strike its fancy, as long as doing so does not violate a contractual agreement between the employer and employee. But as an economic matter, any employer in a competitive industry who acts on prejudices that have no economic merit is an employer who effectively not only rids its own wallet of $20 bills but does so in a way that leaves these valuable assets available to be picked up and used productively – and against it – by its competitors. And $20 bills do not long lay unclaimed.

Here are some slices from Heather’s fine article:

Ms. Pao’s suit is a perfect example of the feminist vendetta against Silicon Valley companies. That vendetta is based on the following conceit: Businesses refuse to hire or promote top-notch employees who would increase their profits, simply because those employees are female. Reality check: Any employer who rejects talent out of irrational prejudice will be punished in the marketplace when competitors snap up that talent. For the feminist line of attack on Silicon Valley to be valid, every tech firm would need to be conspiring in an industrywide economic suicide pact.Kleiner Perkins had devoted considerable time and resources to developing Ms. Pao’s potential. The idea that the firm was simultaneously thwarting her because of her gender and forfeiting its own investment in her is absurd.

….

The market is the best antidote to discrimination. It rewards talent and penalizes prejudice. Silicon Valley, an unprecedented cornucopia of life-transforming innovation, is a shining example of entrepreneurial market forces. Kleiner Perkins might have won this recent skirmish, but Silicon Valley remains in the cross hairs of feminist crusaders and their media allies. Expect companies to load up on bean-counting diversity officers and sexual-harassment training."

Monday, March 30, 2015

Disagreement over Chile’s National School Choice Program

From Andrew J. Coulson of Cato.

"A week ago, the Atlanta Journal Constitution published an on-line op-ed critiquing Chile’s nationwide public-and-private school choice program. In a letter to the editor, I objected to several of the op-ed’s central claims. The authors responded, and the AJC has now published the entire exchange. A follow-up is warranted, which I offer here:

Comment on the Gaete, Jones response to my critique:

Their response consists chiefly of “moving the goalposts”—changing the issue under debate rather than responding to the critique of the original point. The first claim in their original op-ed to which I objected was that “there is no clear evidence that [Chilean] students have significantly improved their performance on standardized tests.” In contradiction of this claim I cited the study “Achievement Growth” by top education economists and political scientists from Harvard and Stanford Universities. That study discovered that Chile is one of the fastest-improving nations in the world on international tests such as PISA and TIMSS—which were specifically designed to allow the observation of national trends over time. It is hard to conceive of clearer evidence that Chilean students “have significantly improved their performance”, contrary to the claim of Gaete and Jones.

To the extent that Gaete and Jones address this evidence at all it is by saying: “it is true that Chile has shown a certain improvement in [its] relative position in PISA scores. But (1) this may say less about Chilean improvements and more about other countries’ relapse.” That is an empirically testable claim. It has been tested, and it is false. As I pointed out in my original letter, prof. Gregory Elacqua has shown that the same pattern of improvement in academic performance is visible on Chile’s own national SIMCE test, which is entirely unaffected by the performance of foreign nations (see chart 1). Moreover, the improvement in Chilean academic achievement noted in the “Achievement Growth” study is not purely relative to other countries but is an objective gain compared to Chile’s own earlier performance.

Chart 1: Same trend in national tests (SIMCE language and math, 4th grade)

Even if that were not the case and Chile were only improving relative to the entire rest of the world because the whole rest of the world was suffering a decline, it would beg the question: what is Chile’s secret that is allowing it to buck this worldwide slump? Certainly it would be wrong to dismiss Chile’s education system out of hand as part of the explanation.

But rather than spending much time trying to dispute this evidence that contradicts their original claim, the authors try to change the subject, proposing that “testing is neither the only nor the best way or criterion to determine the quality of an educational system, it is simply the way favoured by market-oriented systems.” It was also, recall, the very first way in which Gaete and Jones themselves proposed to evaluate Chilean education in their op-ed, with their mistaken claim about a lack of test score improvement. But rather than seriously confronting the evidence that refutes them, the authors choose to change the subject, asserting that: “there are no big differences between the private and public system in the [domestic Chilean] SIMCE [test].” This new claim is entirely beside their original point, which was the trend in academic performance for the nation’s students as a whole.

But, having addressed the authors’ original claim, I have no objection to addressing this new one. The effects of a competitive education system are not limited to—or even chiefly comprised by—differences in performance between the sectors. One the contrary, it is the overall performance of all schools and children that is of interest. Alas, Gaete and Jones seem unaware that increased competition from private voucher schools improves the performance of nearby government schools. This has been shown empirically by Francisco Gallego in his study “When does Inter-School Competition Matter? Evidence from the Chilean `Voucher’ System.”

Next, Gaete and Jones attack Chile’s education system on the grounds that it suffers from an educational gap between its wealthier and poorer students. That it does, but so do other nations. It is more meaningful to ask how Chile compares in this respect to its peer Latin American nations.

Inequality can be measured using several different metrics, one of which is to look at differences in test scores between wealthier and poorer students. These results vary somewhat by subject, grade, and test, but as an example we can look at the PISA test of reading among 15-year-olds. Here, Chile’s achievement gap is statistically indistinguishable from the overall average of all participating countries and significantly smaller than the gaps in most other Latin American countries. Chile’s achievement gap is also significantly smaller than the gaps in the United States, France, Belgium, and several other rich nations (“PISA 2009 Results: Learning to Learn,” Vol. III, Table III A, 2010).

Another way of measuring educational inequality is the average number of years of schooling completed by the wealthiest versus the poorest students. On this point, professor Claudio Sapelli summarizes the evidence for El Mercurio: “Chile has the lowest average educational inequality in Latin America. To measure inequality using the education gap between quintile 5 (richest) and 1 (poorest). In terms of change in this gap in the last 20 years, Chile is among the few countries in Latin America to decrease it.” So, here again, the data on Chile’s education system seem encouraging.

Looking beyond the education system to the broader economy, income inequality has also been falling in recent decades, as has poverty. “The fraction of the population living under the poverty line in Chile fell from 45.1% to 13.7% between 1987 and 2006” (Eberhard & Engel, 2008). Meanwhile, “from 1990 onwards the wage of the 10th percentile [poorest] and the median wage [middle class] grew faster than [that of the] the 90th percentile [the wealthy]” (Eberhard & Engel, 2008)."

Bernanke Says “The Fed Has a Rule.” But It’s Only Constrained Discretion and It Hasn’t Worked

From John Taylor.

"In response to a question about the policy rules bill at Brookings recently, Ben Bernanke remarked that the “The Fed has a rule.” His claim surprised quite a few people, especially given the Fed’s resistance to the policy rules bill, so he then went on to explain: “The Fed’s rule is that we will go for a two percent inflation rate. We will go for the natural rate of unemployment. We will put equal weight on those two things. We will give you information about our projection, our interest rates. That is a rule.” But the rule that Bernanke has in mind is not a rule for the instruments of the kind that I and many others have been working on for years, or that Janet Yellen referred to in speeches over the years, or that Milton Friedman made famous.

Rather the concept that he has in mind is called “constrained discretion,” a term which he dubbed long ago in an effort to distinguish it from the idea of a rule for the instruments such as Milton Friedman’s which he sharply criticized. Bernanke first used the term in a 1997 paper with Rick Mishkin and later in a 2003 speech shortly after joining the Fed board. In fact, it is a concept he has favored from before the time that I first presented the Taylor rule.

It is that all you really need for effective policy making is a goal, such as an inflation target and an unemployment target. In medicine, it would be the goal of a healthy patient. The rest of policy making is doing whatever you as an expert, or you as an expert with models, thinks needs to be done with the policy instruments. You do not need to articulate or describe a strategy, a decision rule, or a contingency plan for the instruments. If you want to hold the interest rate well below the rule-based strategy that worked well during the Great Moderation, as the Fed did in 2003-2005 after Bernanke joined the board, then it’s ok as long as you can justify it at the moment in terms of the goal.

“Constrained discretion” is an appealing term, and it may affect discretion in some sense, but it is not inducing or encouraging a rule as the language would have you believe. Simply having a specific numerical goal or objective function is not a rule for the instruments of policy; it is not a strategy; it ends up being all tactics, all discretion. Bernanke obviously likes the approach in part because he believes “the presumption that the Taylor rule is the right rule or the right kind of rule I think is no longer state of the art thinking.” There is plenty of evidence that relying solely on constrained discretion has in fact resulted in a huge amount of discretion, and that has not worked for monetary policy. David Papell and his colleagues have shown empirically that it is during periods of rules-based policy, rather than periods of so-called constrained discretion, that economic performance has been good."

Sunday, March 29, 2015

Export-Import Bank costly to Pa. businesses

By Daniel Ikenson of Cato.

"If you count yourself among the majority of Americans fed up with the unsavory, business-as-usual, backroom dealing that continues to define Washington, take heart in the fact that the charter of the scandal-prone U.S. Export-Import Bank is set to expire on June 30.

If you are among the misinformed or privileged few who support the bank's reauthorization, how do you justify the collateral damage that Ex-Im inflicts on companies in Pennsylvania and across the country?

Ex-Im is a government-run export credit agency that provides below-market-rate financing and loan guarantees to facilitate sales between U.S. companies and foreign customers. In 2013, roughly 75 percent of Ex-Im's subsidies were granted for the benefit of just 10 large companies - including Boeing, Bechtel, and General Electric - that easily could have financed those transactions without taxpayer assistance.

Supporters characterize the bank as a pillar of the economy, undergirding U.S. export sales that allegedly create more and higher-paying U.S. jobs. But a fatty sheath of willful ignorance has insulated the bank from the scrutiny it deserves. Like all Washington subsidy programs, Ex-Im gives to the few but takes from the many.

When the government subsidizes your competitor's sales but not yours, you are made worse off because your competitor can now offer lower prices or better sales terms than he could have otherwise. Call these the "intra-industry" costs.

Likewise, when the government subsidizes your suppliers' sales to your competitor, you are made worse off because your competitor's costs are artificially reduced, enabling him to charge lower prices or offer better sales terms than he could without the subsidy. Call these the "downstream" costs.

Ex-Im's management and its Washington-savvy supporters have been running a shell game, dazzling Congress with the shiny new export sales it finances while drawing policymakers' attention away from the costs those activities impose on everyone else.

Last year, Delta Airlines finally had enough and complained about Ex-Im loans to Air India, which were granted to enable the foreign carrier to purchase aircraft from Boeing. Delta officials demonstrated how those taxpayer subsidies, made for the benefit of Boeing's bottom line, put Delta at a competitive disadvantage by reducing Air India's capital costs, enabling it to lower fares and compete more effectively with Delta for international travelers. Why should taxpayer dollars be used to promote the interests of one U.S. company over another?

The problem isn't limited to Delta. A recent Cato Institute study estimated the net costs imposed on firms in downstream industries on account of Ex-Im subsidies to firms in supplier industries to be $2.8 billion per year. The study also showed that firms in 80 percent of U.S. manufacturing industries incur costs that exceed the total value of Ex-Im subsidies they may receive. In other words, the average firm in four of every five manufacturing industries is made worse off by the Export-Import Bank.

Pennsylvania is home to hundreds of companies in the industries that have been victimized in precisely the same manner as Delta. The commonwealth's manufacturers of aerospace products, automobile parts, computer network equipment, electrical products, machinery, semiconductors, telecommunications equipment, and more can be counted among the victims because their suppliers secured Ex-Im dollars to subsidize sales to foreign customers.

Here are a few examples of Pennsylvania businesses that bear the costs of Ex-Im's subsidies: Herley Industries, a search-and-navigation equipment manufacturer in Lancaster with more than 1,000 employees; Williamsport-based semiconductor manufacturer Primus Technologies, with about 470 workers; telecommunications equipment producer Compunetix, with 360 workers in Monroeville; and General Carbide Corp., a metalworking machinery manufacturer with 160 employees in Greensburg.

There are many more.

According to the Cato study, the five broad manufacturing sectors incurring the largest downstream costs from Ex-Im's subsidies account for 40 percent of Pennsylvania's manufacturing economy. Included among the 10 most heavily burdened sectors are the state's first, second, fourth, and sixth most important manufacturing industries: chemicals; food, beverage, and tobacco; primary metals; and computers and electronics, respectively.

The Export-Import Bank temporarily benefits some companies in a conspicuous manner. But it does so by quietly burdening often unwitting American companies in downstream industries. Delta and others have cried foul. Pennsylvania's business victims should speak up as well."

The National Road was built with stone (crushed and solid), and it became one of the most expensive roads, if not the most expensive, in the United States in the early 1800s

From Cafe Hayek.

"from page 5 of Burt and Anita Folsom’s 2014 volume, Uncle Sam Can’t Count; here they are discussing Uncle Sam’s early-19th-century infrastructure project popularly known as “the National Road - a 620-mile- (1,000km-) long road extending westward from Cumberland, Maryland to Vandalia, Illinois (footnotes excluded):

Because the road was a government project, no one had an incentive to keep costs down. The National Road was built with stone (crushed and solid), and it became one of the most expensive roads, if not the most expensive, in the United States in the early 1800s. For example, the privately funded Lancaster Turnpike, also built with stone, cost $7,500 per mile – versus $13,000 for the National Road. The builders of the Lancaster Turnpike were spending their own money and had to spend it wisely, or else the tolls wouldn’t cover their expenses. Those in charge of the National Road, by contrast, were political appointees, described by one newspaper editor as being “as numerous as the locusts of Egypt.” Funded with taxpayer dollars, the National Road never charged tolls and never made a profit.At the same time, because no one individual owned the National Road, no one had a strong stake in building it well, or preserving it once it was finished. Almost every firsthand account describes the road’s shoddy construction. Even in its heyday it was never fully paved; it always had gaps and always needed repairing."

Saturday, March 28, 2015

Regulations May Have Played A Role In Inequality

See What's new since 1982? by Scott Sumner. Excerpts:

"When I moved to Boston in 1982, no one talked about the declining share of national income going to labor. Or increasing income inequality. Now these are the hottest topics in economics. Much of the discussion seems to implicitly suggest that there is some sort of "mystery" to be explained. Perhaps corporations are getting better at lobbying in Washington. Or maybe there is cultural change that makes CEOs bolder in demanding high pay.

I find those sorts of explanations to be unsatisfactory. Too vague."

"I believe that major societal changes don't just happen randomly, they have causes. Here are three reasons that others have pointed to:

1. The growing importance of rents in residential real estate.

2. The vast upsurge in the share of corporate assets that are "intangible."

3. The huge growth in the complexity of regulation, which favors large firms.

Kevin Erdmann did some very important posts on the share of income going to capital, which haven't gotten anywhere near the attention they deserve. Here are a few excerpts, but read his whole series of posts:

We start with Profit (the blue line at the bottom). I have extended the time frame further back. The green line represents all returns to corporate capital, both to debt and equity. The debt portion peaked in the early 1980's when corporate leverage was at its highest. When we make this correction, we find that corporate returns to capital have been flat for 40 or 50 years. If we add in proprietors' income, we find that returns to capital have been flat or declining for a century. From 1929 to about 1985, there was a trend of profit claims moving from proprietors to creditors. From 1985 to the present, there was a trend of profit claims moving from creditors to equity owners. But, there is no trend of increasing total returns to capital over the past 30 years.So in recent decades the rising equity income is offset by falling interest income, leaving total income to the corporate sector fairly stable, as a share of GDP. But then why is labor losing out? It turns out that more income is going to the residential real estate industry, but it's implicit income from rents:

First, this is a little tricky, because 60% of American households own their homes. So, in effect, this is a measure of rent we are paying ourselves. Or, put differently, this is a measure of the income share we capture because home ownership tends to provide excess returns.The trend in Compensation has dropped from about 57% in 1970 to about 53% - a 4% drop. But, the trend in Rent + Compensation has dropped from about 59% to 57%. Rental income explains about half the drop in Compensation Share, and in fact, accounts for more than all of the drop in Compensation Share since the previous low point in 2006.To the extent that Rental Income supplements Compensation, this income is probably distributed mostly to middle and upper-middle class households. So, both the level and the distribution of household Compensation Share are probably helped by reducing excess returns to Rental Income."What about corporations? We all know that the capital-intensive businesses of yesteryear like GM and US steel are an increasingly small share of the US economy. But until I saw this post by Justin Fox I had no idea how dramatic the transformation had been since 1975:

The rise of companies like Apple, Facebook and Uber affect the economy in two ways. Intellectual property rights create more monopoly power than manufacturers of TVs and refrigerators had back in the 1960s, and this boosts corporate profits. In addition, the individuals with the creative ideas and/or the financiers who picked the winners in the high tech race can make much larger personal incomes than a CEO at an appliance maker in the 1960s. How hard is it to figure out how to make washing machines? How hard is it to figure out the next WhatsApp? These are totally different skills.

However, I'd guess that it's not just about high tech. We've also seen companies like Starbucks do increasingly well against the local corner coffee shop. There could be lots of reasons for this, but one might be the rapid growth in regulations. When regulations are highly complex, there are enormous economies of scale in dealing with the complexities. This favors larger firms. And as this article at Free Exchange points out, anything that favors the growth of larger firms tends to increase inequality:

The standard explanation says that technology plays a big role: modern economies require more skilled workers, raising the pay premium they can demand. A new paper* by Holger Mueller, Elena Simintzi and Paige Ouimet adds a new and intriguing wrinkle to this: the rising size of the average firm. Economists have long recognised that economies of scale allow workers at bigger firms to be more productive than those at smaller ones. That, in turn, allows the bigger firms to pay higher wages. This should not, in theory, cause a rise in inequality. If the chief executive and cleaner at a larger firm are both paid 10% more than their counterparts at a small firm, the ratio between their wages--and thus the overall level of inequality--should remain the same.But the paper shows that the benefits of scale are not shared equally among all workers. Using data on wages at British firms, they divide workers into nine groups according to how skilled they are. Over time, they find that the proportional difference in wages between the groups grows as firms get bigger. This trend is driven entirely by a rising gap between wages at the top compared with the middle and bottom of the distribution. As the authors note, this is very similar to the trend in income inequality in America and Britain as a whole since the 1990s, when pay for low and median earners began to stagnate (see chart).What do all three of these explanations have in common? Regulations. Building restrictions are increasing rental income as a share of national income. Intellectual property rights are barriers to entry that tend to create a winner-take-all situation (although other factors like network effects also play a role.) And other types of regulations (financial, human resources, etc.) are especially burdensome for small firms, and this favors the growth of inequality-intensive large firms."

Minimum wage increase causes cuts in hours, jobs, and services in S. Dakota

From Mark Perry.

"NC1-TV in Rapid City, SD is reporting in the video above that:

Changes are coming for workers at South Dakota’s six public universities. The schools are reigning in hiring and cutting back hours and services as a result of the new $8.50 minimum wage that voters approved in November. The Regents predicted the wage hike would increase costs by about $970,000 over a full year. Some universities have reduced the availability of services such as building hours.MP: What? A government-mandated minimum wage leads to: a) reducing hiring, b) reduced hours for workers, and c) reduced hours of service? As an economist, I’m shocked!"

Friday, March 27, 2015

Climate Sensitivity and Environmental Worries Are Trending Downward

From Patrick J. Michaels and Paul C. "Chip" Knappenberger of Cato.

"More evidence this week that high-end forecasts of coming climate change are unsupportable and Americans’ worry about environmental threats, including global warming, is declining. Maybe the general public isn’t as out of touch with the science as has been advertised?

First up is a new paper by Bjorn Stevens from Germany’s Max Plank Institute for Meteorology that finds the magnitude of the cooling effect from anthropogenic aerosol emissions during the late 19th and 20th century was less than currently believed, which eliminates the support for the high-end negative estimates (such as those included in the latest assessment of the U.N.’s Intergovernmental Panel on Climate Change, IPCC). Or, as Stevens puts it “that aerosol radiative forcing is less negative and more certain than is commonly believed.”

This is important, because climate models rely on the cooling effects from aerosol emissions to offset a large part of the warming effect from greenhouse gas emissions. If you think climate models produce too much warming now, you ought to see how hot they become when they don’t include aerosol emissions. The IPCC sums up the role of aerosols this way:

Despite the large uncertainty range, there is a high confidence that aerosols have offset a substantial portion of [greenhouse gas] global mean forcing.The new Stevens’ result—that the magnitude of the aerosol forcing is less—means the amount of greenhouse gas-induced warming must also be less; which means that going forward we should expect less warming from future greenhouse gas emissions than climate models are projecting.

Researcher Nic Lewis, who has done a lot of good recent work on climate sensitivity, was quick to realize the implications of the Stevens’ results. In a blog post over at Climate Audit, Lewis takes us through his calculations as to what the new aerosols cooling estimates mean for observational determinations of the earth’s climate sensitivity.

What he finds is simply astounding.

Instead of the IPCC’s estimate that the equilibrium climate sensitivity likely lies between 1.5°C and 4.5°C, Lewis finds the likely range to be 1.2°C to 1.8°C (with a best estimate of 1.45°C). Recall that the average equilibrium climate sensitivity from the climate models used by the IPCC to make future projections of climate change and its impacts is 3.2°C—some 120% greater than Lewis’ best estimate. But perhaps even more important than the best estimate is the estimate of the upper end of the range, which drops from the IPCC’s 4.5°C down to 1.8°C.

This basically eliminates the possibly of catastrophic climate change—that is, climate change that proceeds at a rate that exceeds our ability to keep up. Such a result will also necessarily drive down estimates of social cost of carbon thereby undermining a key argument use by federal agencies to support increasingly burdensome regulations which seek to reduce greenhouse gas emissions.

If this Stevens/Lewis result holds up, it is the death blow to global warming hysteria.

Which brings us to the last results of Gallup’s annual poll gauging the level of environmental concern among Americans—something the polling agency has been keeping track of since the late 1980s.

Here’s Gallup’s summary of this year’s results:

Americans’ concern about several major environmental threats has eased after increasing last year. As in the past, Americans express the greatest worry about pollution of drinking water, and the least about global warming or climate change.And Gallup’s full write-up includes this gem:

Importantly, even as global warming has received greater attention as an environmental problem from politicians and the media in recent years, Americans’ worry about it is no higher now than when Gallup first asked about it in 1989.

Says something about the effectiveness of the climate alarm campaign.

The full set of questions and results are available here. You ought to have a look!"

Would you choose to be you today or John D. Rockefeller a century ago?

See Richer than Rockefeller? by David Henderson EconLog.

"This is the longest time I've gone without posting, other than when I'm on vacation at my cottage in Canada in August. I was traveling and my computer was being repaired after I got back.

Thursday, March 26, 2015

ethanol has about one-third less energy than an equal volume of gasoline

See Root Cause of Ethanol ‘Blend Wall’? Consumers Don’t Like Rip Offs by Marlo Lewis of globalwarming.org. Excerpt:

"Although ethanol is cheaper by the gallon than regular gasoline, ethanol has about one-third less energy than an equal volume of gasoline. On an energy-adjusted (bang-for-buck) basis, regular gasoline is almost always the better buy than ethanol. Consequently, the higher the ethanol blend, the worse mileage your car gets, and the more money you spend to drive a given distance.

FuelEconomy.Gov, a Web site jointly administered by EPA and the Department of Energy (DOE), calculates how much a typical motorist spends in a year to fill up a flex-fuel vehicle with either E85 or regular gasoline. The exact bottom line changes as gasoline and ethanol prices change. The big picture, though, is always the same: Ethanol is a net money loser for the consumer.

At today’s prices, depending on make and model, it costs an extra $900, $1,200, $1,600, or even $2,400 annually to run a flex-fuel vehicle on E85 rather than regular gasoline. Those hefty price differences — not oil company machinations or EPA indecision — are the principal barrier to market penetration of E85 and other high-ethanol blends.

Even if everybody owned a flex-fuel vehicle, and every service station installed E85 blender pumps, few willing customers would buy the fuel. Lower energy content, inferior fuel economy, and higher consumer cost are the root cause of the blend wall. The same factors also explain why the ”choice” to buy ethanol must be mandated. After all, if ethanol were a great deal for consumers, why would we need a law to make us buy it?"

we are spending thousands of dollars worth of water to grow hundreds of dollars worth of almonds and that is truly nuts

See The Misallocation of Water at Marginal Revolution. Farmers get subsidized prices for water.

"One of the most remarkable discoveries of economics is that under the right conditions competitive markets allocate production across firms in just that way that minimizes the total costs of production. (You can find a discussion of this remarkable property in Modern Principles. See also this MRU video.)

One of the necessary conditions for this result is that firms must face the same input and output prices. If one firm is subsidized and another taxed, for example, then resources will be misallocated and total costs will increase. In a pioneering paper, Klenow and Hsieh measure misallocation across firms in China, India and the United States and they find that micro misallocations can have large, macroeconomic effects. In particular, if capital and labor were allocated as well in China and India as they are in the United States then output in those countries would double.

We can get some intuition for the costs of resource misallocation by looking at water in California. As you may have noticed at the grocery store, almonds are in demand right now whether raw or in almond milk. Asian demand for almonds is also up. As a result, in the last 10 years almond production in California has doubled. That’s great, except for the fact that almond production uses a huge amount of water and water in CA is severely mispriced and thus misallocated.

In my previous post, I pointed out that agriculture uses 80% of the water in California but accounts for less than 2% of the economy. So how much water does almond production alone use? More water is used in almond production than is used by all the residents and businesses of San Francisco and Los Angeles combined. Here’s a chart from Mother Jones:

(Aside: Some of this water is naturally recycled so net use is likely somewhat lower but a lot of water in California is now being pumped from the aquifer and that water isn’t being replenished.)

At the same time as farmers are watering their almonds, San Diego is investing in an energy-intensive billion-dollar desalination plant which will produce water at a much higher cost than the price the farmer are paying. That is a massive and costly misallocation of water.

In short, we are spending thousands of dollars worth of water to grow hundreds of dollars worth of almonds and that is truly nuts."

Subscribe to:

Comments (Atom)