Evaluating the free market by comparing it to the alternatives (We don't need more regulations, We don't need more price controls, No Socialism in the courtroom, Hey, White House, leave us all alone)

Thursday, September 1, 2022

Capitalism, Slavery, and the Industrial Revolution

"This post is the first installment of a trilogy. Part I, below,

covers the debate up to the late 1980s. The second will run through

debates among economic historians since 1990, focusing especially on

exchanges between Harley, Findlay and O’Rourke, McCloskey, and Zahedieh.

The last will survey the economics work on the Atlantic economy and

slave trade up to the present (literally, this year).

This series is not about

the economics of plantation slavery, which was brutal, profitable, and

fully compatible with capitalism. It’s about the role that slavery

played in endogenously generating modern growth in Britain. With that in

mind, the TL;DR:

Profits from the slave trade were not demonstrably large with respect to British national income.

While they were pretty big compared with industrial

investment, supposing them to be significant requires implausibly

assuming that all profits were saved and that all profits went into

industry, rather than land or trade/services.

The Jamaican plantation economy did generate substantial wealth, but for the same reasons in (2) it’s not clear that they actually financed much investment. Many Jamaican planters repatriating money to Britain did what you’d expect them to do—buy estates.

Moreover, it’s possible that the wealth generated by the Jamaican plantations was completely offset by A) elevated sugar prices due to mercantilist tariffs and B) the costs of Jamaica’s garrisons and naval defense.

Debating

Williams’ financing channel was unlikely to prove fruitful anyway;

capital accumulation probably did not cause British industrialization,

given the modest set-up costs of even large factories.

By

the 1980s, most pro-Williams historians had given up on fighting about

“small ratios” in favor of an “Atlanticist” view emphasizing British

exports to New World plantation economies rather than investment

capital; this view was more or less accepted by several anti-Williams

historians.

Great

Transformations is a reader-supported publication. To receive new posts

and support my work, consider becoming a free or paid subscriber.

In

August 1962, an Oxford historian became the first Prime Minister of

newly-independent Trinidad and Tobago. He was the country's only Prime

Minister until 1981, winning an unbroken string of elections up to his

death at the age of 69, by which time he’d been dubbed the “Father of

the Nation.”

Among economic historians, Eric Williams is better known for his 1938 Ph.D. thesis, published in 1944 as Capitalism and Slavery.

Williams, a Marxist, argued that slavery catalyzed British

industrialization during the 18th century and that "the monster

[capitalism] then turned around and destroyed its progenitors

[slavery]"—manufacturers no longer needed the West Indian plantations

and abolished an obsolete slavery. Williams wanted to show that

abolitionism played a minor role in emancipation (the Marxist elevation

of the material over the ideological). But economic historians have

mostly focused on his preliminary claim, which we now call the "Williams

thesis": that Britain's involvement in the slave-based Atlantic economy

caused the Industrial Revolution.

For a short book, Capitalism and Slavery

ranges over an enormous variety of topics, so it's hard to pick out the

core tenets of the “Williams thesis,” other than the basic association

between slavery and British industrial development. Williams focused on

surplus capital, drawing a channel from profits derived in the Atlantic

trade and the plantation economy to investment: "the profits obtained

provided one of the main streams of that accumulation of capital in

England which financed the Industrial Revolution" and "supplied part of

the huge outlay for the construction of the vast plants to meet the

needs of the new productive process and the new markets."

Capitalism and Slavery was, as Kenneth Morgan (2000)

charitably suggests, written "at a time when statistical presentation

in economic history was much less rigorous than today." He means that

Williams' approach was scattershot. I've isolated three parts of the

original Williams thesis: 1) that profits from the slave trade were an

irreplaceable source of industrial finance 2) that the wealth of

Caribbean planters played a similar role 3) that the Atlantic economy

was, in general, important for British development. To support 1),

Williams pushed a 30 percent figure for profits on the slave trade,

which would have been more than twice the "normal" rate for the day. His

data was totally inadequate for the purpose, consisting largely of

lists of rich Britons who'd somehow made at least a pound or two off

slavery. So there was a lot of room for early cliometricians—who cut

their teeth with controversial debunkings of historical theories—to

challenge his expansive claims.

The Williams thesis

is economic history's longest-running debate. And because slavery is

often perceived as capitalism's original sin, it just won't go away.

Williams has been revived in the twenty-first century by the popular

book Power and Plenty

by Ronald Findlay and Kevin O'Rourke, as well as recent interventions

by economists Stephen Redding, Stephen Heblich, and Hans-Joachim Voth.

We're starting in 1944, and with almost eighty years of terrain to

cover, we're going to have to split this up into three posts. The first

will tackle the initial (and heated) debates over points 1) and 2),

ending with the work of Barbara Solow in the late 1980s. The second will

explore the economic history literature since Solow, focusing on the

evolution of the Williams thesis to cover broader assertions of the

importance of the Atlantic economy (3). The third and final version will

survey the recent work of economists in raising the ghost of Williams

in a new conceptual garb, based on models of agglomeration economies and

financial frictions.

The trade profits and plantation

wealth debates happened sort of simultaneously, so we'll weave between

them as we go. What we'll see is that the original formulation of the

Williams thesis was basically completely wrong, and by the early 1980s

that had become pretty obvious. But a revived version, emphasizing the

importance of the broader “Atlantic system” to British

industrialization, had replaced the old profits contretemps and become

orthodox by 1987.

Slave Trade Profits

At

core of the Williams thesis is an argument that profits from the slave

trade launched British industrialization by contributing to capital

formation. This claim rests on answers to three empirical sub-questions:

1) how big were the profits relative to other industries and the

overall size of the economy? 2) did profits rise prior to

industrialization? 3) did slave trade profits specifically make a

difference? The first phase of the debate centered on 1). Williams

himself attempted no real analysis of systematic profits, instead

adducing specific instances in which slave traders had reaped enormous

gains—like John Tarleton, who’d turned £6,000 in 1748 into almost

£80,000 by 1783. As I noted above, Williams guessed that average profits

were 30 percent. As his detractors showed, he was totally wrong.

The

first critiques of Williams' profit-based arguments came from Bradbury

Parkinson (1951), an accountant, who demonstrated how to actually read

slavers' account books. In Hyde et al. (1952), he and two co-authors

showed that outcomes for Liverpool slave traders were highly varied,

ventures were risky, and partnerships broke up frequently, all of which

lowered returns. The main series used for this project, the 1757-84

accounts of William Davenport, was later studied by David Richardson (1975).

Richardson disaggregated the 67 extant voyage accounts in the Davenport

records and found that 49 were profitable and 18 were losses. Moreover,

he found that the average profit was 8.1 percent per annum,

substantially lower than Williams' back-of-the-napkin estimate.

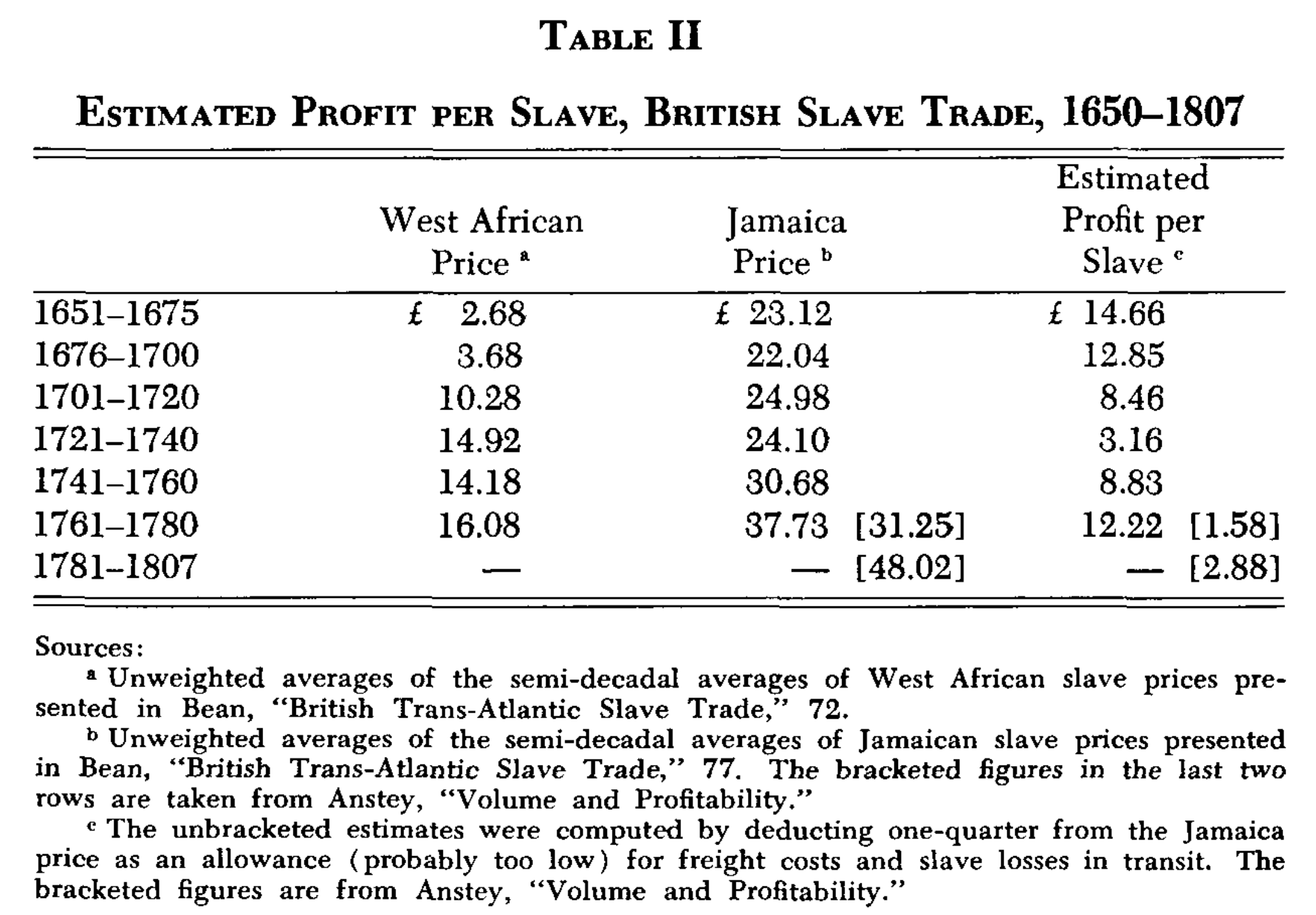

Roger Anstey's The Atlantic Slave Trade and British Abolition, 1760-1810

sought to extend the profit analysis beyond single voyages in a

constricted time period. He matched data from the voyage accounts to the

numbers and prices of slaves sold in the Americas, concluding that

profits rose from 8.1 percent in 1761-70 to 13.4 percent in 1781-90

before falling back to 3.3 percent in 1801-7. The average annual profit

during those fifty years was 10.2 percent, slightly higher than

Richardson's figure, but still much lower than Williams'.

Thomas and Bean (1974)

devised a third and final approach to minimizing the profits of the

slave trade, which was to theoretically examine the market structure of

each stage in the transport of slaves from Africa to America. Since all

stages of the commerce open to Europeans could be freely entered, they

argue that levels of competition were extremely high and that all inputs

but the slaves themselves were supplied perfectly elastically. So

marginal firms should only have experienced temporary periods of

non-zero profits. In a phrase that must have annoyed the heck of their

adversaries, Thomas and Bean write that "[t]he 'invisible hand'

eliminated any long-run economic profits." Indeed, the potential profits

were actually passed on to the African slavers—the "fishers of

men"—themselves.

Stanley Engerman (1972)

asked the macro-question (3): "to what extent was the over-all level of

investment in society raised by the profits of the slave trade?"

Engerman noted that Williams' model, unlike his own neoclassical "new

economic history" reasoning, assumed that resources weren't fully

employed; so Williams was led to count any resources (e.g. capital and

labor used in shipping and on plantations) used in the slave trade as

gains. His procedure is simple: count the number of slaves exported,

estimate the profits per slave, multiply the two figures, and compare

the result to the investment share of British national income.

Engerman's

profit-per-slave figures were probably (intentionally, to bias the

analysis against himself) gross over-estimates, as he just subtracted

1/4 the Jamaica price to account for costs. Even using the overstated

profit numbers, slave profits were usually less than .5% of British GDP,

and less than .1% using Anstey's more accurate estimates. Assuming a 5

percent investment rate and that slave traders saved every penny of

their returns, the slave trade contributed at most 10.8 percent of

British capital formation at its peak and as little as 2.4 percent at

its trough. Only if one assumes that A) Engerman's upper-bound estimates

are correct B) all profits were saved and C) all saved profits went

into industry do you get a significant outcome—that slave profits peaked

at 54 percent of industrial and commercial capital formation. Using

Anstey's empirically derived figures, however, Engerman comes out with a

much smaller (but still inflated!) 7 percent. Anstey himself conducted a

similar exercise three years later and found that profits from the

slave trade accounted for .11 percent of national investment.

In

short, the first wave of new economic history studies to tackle the

slave trade portion of the Williams thesis effectively shattered it.

A Plantation Revolution?

Williams

also alleged that the wealth of the Caribbean plantations, obviously

derived from slavery, was a second source of funds for British

industrialization. The West Indies were the richest part of the first

British Empire, valued at £50-60 million in 1775 and £70 million in

1789. The population of the region rose by 40 percent from 1750 to 1790,

sugar production by 11 percent, and exports to Britain by 9 percent.

Once again, Williams amassed examples, this time of conspicuously

wealthy Jamaican planters who invested their savings in British

industry. They included Richard Pennant, a Liverpool MP who put the

proceeds from his 600-slave, 8000-acre plantation into slate quarries in

North Wales, and the Fuller family, whose interests included Jamaican

estates, charcoal ironworks, and gun foundries.

But Williams made

too much of his already-small sample. Richard Pares (1950) showed that

William Beckford, a millionaire who owned 14 sugar plantations and over

1000 slaves, invested little of his vast wealth in British industry.

Many others, like John Pinney, were content with channeling funds into

government securities and land. It's also unclear how much Jamaican

money actually came back to Britain; some historians have alleged that

it only came back with emancipation, which would be far too late to play

the role that Williams allots it.

Richard B. Sheridan's "The Wealth of Jamaica in the Eighteenth Century"

(1965) examined records of Jamaican inventories and found that their

average value rose from £3819 in 1741-5 to £9,361 in 1771-5, a movement

almost entirely driven by increases in the number (2x) and price (+76%)

of slaves. He valued Jamaica's sugar estates at £18 million sterling,

which sent an annual income flow to absentee planters and merchants of

£1.5 million—amounting to 8-10 percent of British national income. That

would be quite a lot! But his analysis was, well, imperfect. Since

Sheridan had no aggregate data on financial flows between the colonies

and the capital, his line of argument is essentially: 1) planters were

rich 2) riches were produced by slaves 3) that money must have gone back

to Britain 4) especially into British industry and 5) that this funding

proved the critical margin in establishing new enterprises. As you can

tell, there are lots of assumptions here!

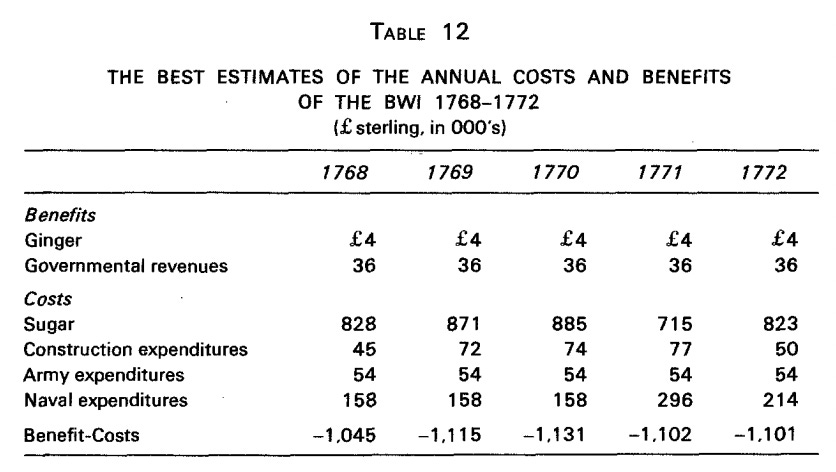

Surprisingly,

Robert Thomas (1968) critiqued Sheridan's analysis without touching

assumptions 1-5. Instead, he proposed a cost-benefit analysis of

Britain's possession of the West Indies for the British consumer.

Warships and garrisons were expensive (an average first-rate ship, in

John Brewer's oft-quoted example, could cost 10 times a large factory),

as were the preferential tariffs granted to Jamaican planters to protect

the imperial sugar market. Thomas actually felt that Sheridan had underestimated

the value of the West Indies, but that this was both totally irrelevant

by comparison with Britain's overall wealth and a poor return on

defense costs.

Thomas asks what the counterfactual return

to investing this wealth (£37 million) gradually in the British economy

might have been; picking out the lower-bound 3.5 percent rate on

risk-free consols to bias his own estimate downward, the number to beat

was £1.295 million. But Sheridan didn't account for the elevated prices

that consumers paid for the discriminatory sugar tariff, which set

consumers back £383,250 per annum, or the massive costs of defense

(£115,000 on troops and £315,895 for ships). Deducting these sums from

the annual total left only £660,750 in social return, or 2 percent per

annum. By Thomas's logic, Britain would’ve had higher income by just

buying riskless assets.

Sheridan (1968)

replied that Thomas had overstated the size of the non-sugar staples

sector and thus the wealth of Jamaica/the West Indies, artificially

reducing the return on capital. He also adduced a list of "invisible"

sources of profits like insurance, remittances via North America,

bullion from the entrepot trade, and sales of Jamaican industry that

altogether raised his rate of return to 8.4 percent, even including

Thomas's cost deduction.

Coelho (1973),

meanwhile, backed Thomas, arguing that the high import prices on

Caribbean sugar diverted resources and defense costs drained £1.1

million per annum out of Britain. Capital was being transferred from

Britain to Jamaica—inverting the Williams thesis entirely! It was the

increasing efficiency of the British economy during the Industrial

Revolution that made the West Indies a profitable place to invest, and

not the other way around.

Source: Coelho (1973)

So

why did Britons submit to the planter monopoly? Coelho (like Ogilvie's

explanation for guild persistence) blamed regulatory capture. Since the

primary beneficiaries of the colonial system were the powerful

plantation and mercantile interests, they had the lobbying power to keep

Parliament on their side. Indeed, many planters ended up

as MPs themselves, including the aforementioned Beckford and Pennant.

It was thanks to the West India interest that Britain kept Canada, and

not Guadaloupe, at the end of the Seven Years' War; the planters feared

the consequences of increased (and highly efficient) competition in the

imperial trading system.

Enter Solow

The plantation debate then went quiet, but in 1981,

Joseph Inikori (get used to seeing his name) attacked the low-profit

position hacked out by the new economic historians of the '70s. Inikori

was annoyed with Thomas and Bean. Rather than an efficient market with

free entry, he asserted, the slave trade was noncompetitive, dominated

by fewer than a dozen top firms with much higher productivity than their

peers. This small, closed group was able to exploit the inequities of

market structure—inelastic supplies of trade goods and credit—to earn

monopolistic profits of up to 50 percent, well in excess of Williams'

exaggerated guess and several multiples of the 10 percent figure agreed

on by Anstey and Richardson. Inikori discards the Davenport accounts,

for which he only finds a maximum of 14 percent profits, on the grounds

that Davenport had ignored non-British markets and used smaller ships

than the bigger traders who appeared after 1780. Inikori also attacked

Anstey for using an excessively low slave price and volume.

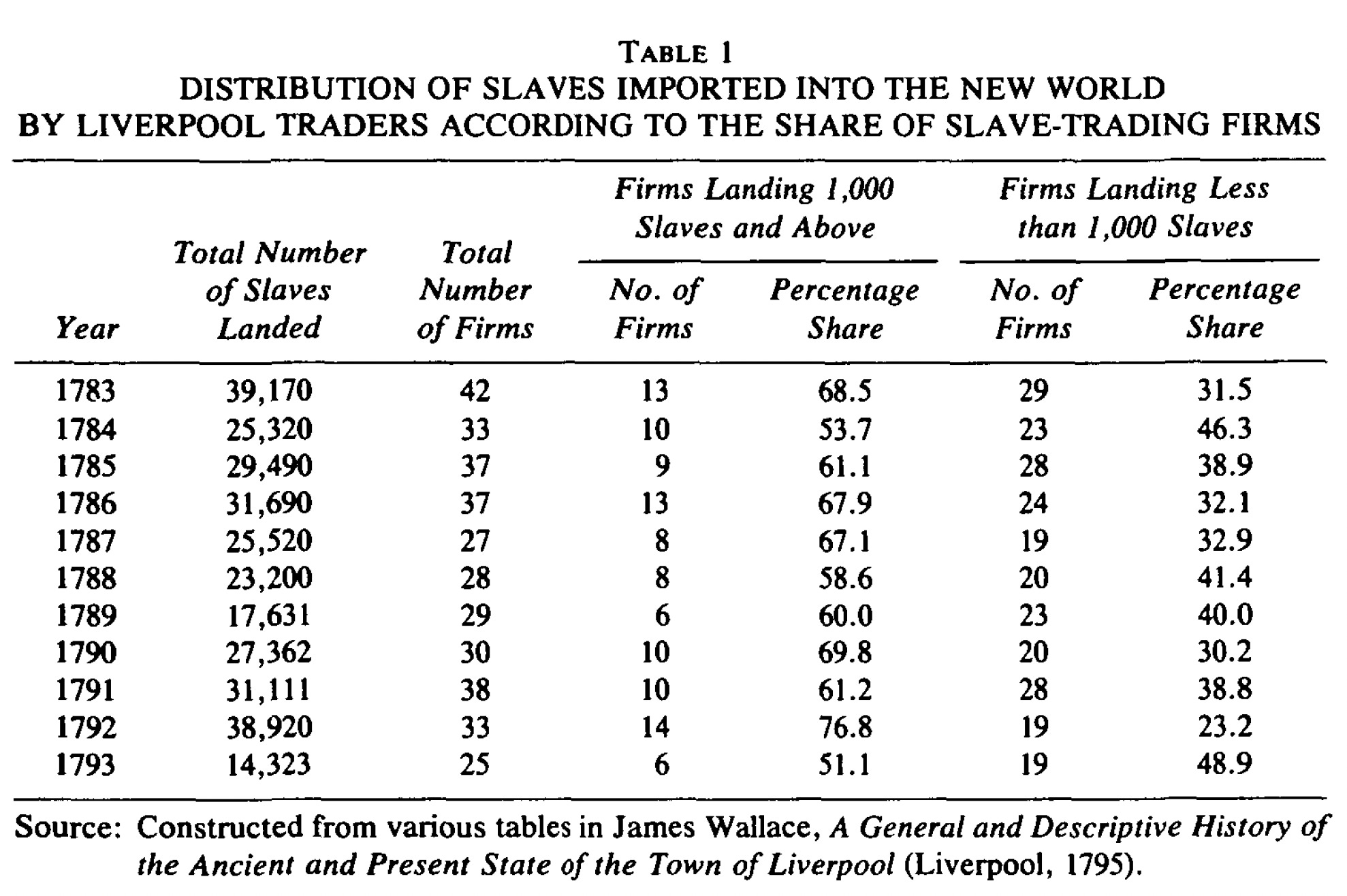

Anderson and Richardson (1983)

returned serve with a comprehensive critique of Inikori's analysis.

Inikori based his average profit calculations on a sample of just 24

voyages; thus a few key observations—five voyages fitted out by just one

firm, Thomas Leyland & Co. between 1797 and 1805, that earned 71

percent returns—could skew the results. Moreover, successful firms were

more likely to have preserved records, creating an upward bias. The

remaining nineteen earned just 12 percent per venture,

lower than in the Davenport sample. In focusing on venture rather than

annual profits, moreover, Inikori ignored the substantial delays that

investors faced in getting their money back. The most successful voyage

in Inikori's sample, that of the Lottery in 1802, made a huge venture profit of 138 percent. But few of the proceeds were collected until 1811, nine years

after the ship sailed! Anderson and Richardson argue that traders

thought on the basis of annual return on capital, and that considering

time factors profits were substantially lower. Moreover, Inikori's

claims about concentration were pretty ephemeral—the largest eight firms

in Liverpool controlled just 58 percent of investment, which is by no

means exceptional. And as the table attached shows, there were a ton of

little firms surviving alongside the large ones with high rates of

turnover, indicating the possibility of entry.

Inikori (1983)

responded that Anderson and Richardson failed to address his contention

that the big firms did better in normal times and then made their

fortunes in boom periods, but he himself avoided the essential point

that traders rose and fell with the times, and that marginal firms were

able to offer effective competition.

William Darity (1985)

then entered and lambasted everyone. He argued that the "market

structure" debate was pointless; bickering over the amount that excess

actual exceeded "normal" profits gave no indication of how big those

profits really were, and using primary sources to deduce profit levels

was fraught by the "Darwinian" selection of successful traders'

accounts. But Darity still thought profits were large. Reviewing the

debate between Inikori and Anstey, he showed that the estimated rate of

return was a function of slave prices, shipping tonnage (proxy for

outlay costs), volume of slave imports, and the fraction of the voyage's

value that returned to England as trading goods. Increasing the number

of slaves imported to 1.9 million and the price to £45, estimated

profits could be as high as 30.8 percent, very much in Williams

territory.

Barbara Solow (1985)

continued the revisionist turn with an attack on Engerman (1972). She

does not contest his figures but rather argues that his maximally

exaggerated estimate (all slave trade profits invested in industry) in

which profits represent 39 percent of industrial and commercial

investment is actually very large. For context, no single industry in

the modern United States has made a contribution of equivalent scale.

That's right, but it's totally irrelevant because of the implausible

assumptions involved in creating this upper bound. Sure, if trading profits were large, if all wealth was invested, and if all

that investment went into industry, then there might be a case for

Williams. But we know that the first is uncertain and the latter two are

just flat-out wrong. So I don’t really see the point of this critique.

More

convincingly, she adds that if Sheridan's West Indies profits are added

to Engerman's total, then slave-related commerce could have contributed

5 percent of national income, or nearly 100% of gross investment. From

this perspective, she suggests that the Williams thesis is irrefutable,

if not provable. I guess. But that still doesn’t deal with the Engerman

assumptions. There’s zero reason to suppose that planters were

especially likely to invest all, or even most,of

their savings in industry. Finally, she uses a simple model to show that

reinvesting the capital sunk in slave enterprises into the British

economy would have reduced domestic profits, investment, and thus

national income. This exercise is entirely speculative and I’m not sure

why you should believe that the effect was of a substantial magnitude.

David Richardson (1987a)

ripped the scab off the wound of the profits debate with a further

analysis of the market structure and internal workings of the slave

trade. He argued that slaves were expensive to transport and subject to

high and highly variably levels of mortality during the Middle Passage,

which, combined with the competitive market structure (sure to incite

controversy) should have limited profits below 10 percent. Darity (1989)

responded by basically repeating his 1985 points in slightly more muted

fashion (abandoning, for example, the inflated number of slaves

transported from 1760-1800) and criticizing the low slave price assumed

by Richardson. Richardson (1989)

in turn replied that Darity had basically just copied Inikori and

argued that the latter's high price estimates were derived from an

overestimate of the share of slaves sold in foreign markets, where they

fetched higher prices. He also noted the irony of Darity's claim that

the profits debate was a "diversion" while still leaping into it once

again.

Inikori, Darity, and Solow have one thing in common:

though they can't resist bickering about profits, they all rightly

disdain the debate as a red herring. In a remark that presages the later

development of his broader theories, Inikori (1981), for example,

writes:

[T]he emphasis on profits in the

explanation of the role of the slave trade and slavery in the British

industrial revolution is misplaced. The contribution of

the slave trade and slavery to the expansion of world trade between the

fifteenth and nineteenth centuries constituted a more important role

than that of profits. The interaction between the

expansion of world trade and internal factors explains the British

industrial revolution better than the availability of investible funds.

This is the more so because it is now known that industries provided

much of their investment funds themselves, by plowing back profits. In

other words, capital investment during the years leading to the

industrial revolution was related not so much to the rate of interest on

loans (depending on the availability of investible funds) as to the

growth of demand for manufactured goods, which provided both the

opportunity for more industrial investment and the industrial profits to

finance it.

Darity also focused on colonial

commerce, arguing that "[i]t was not profitability or profits from the

slave trade that were essential in Williams's theory, but that the

American colonies could not have been developed without slavery" and

labeling the profits debate a "numbers game" and a "diversion." Finally,

Solow proposed that slavery "made more profits for investment, a larger

national income for the Empire, and a pattern of trade which

strengthened the comparative advantage of the home country in industrial

commodities." Indeed, Engerman himself had pointed out the failings of

his own neoclassical approach to determining the role of the slave

trade, admitting that

It is rather clear that a

basically static neo-classical model cannot provide a favorable outcome

for arguments such as those of Eric Williams. That form of argument

depends upon sectoral impacts resting on various imperfections in

capital and other markets, and upon the characteristics of specific

income recipients.

For whatever reason, then, the

participants in the Williams debate accepted that the old arena of

debate either was no longer or had never been productive. By 1985,

Williams' own supporters had essentially abandoned the original thesis

in favor of a new line of argument emphasizing trade and the Atlantic

economy.

Toward the Atlantic Economy

The

"Atlantic economy" focus of the 1980s generation wasn't a coincidence.

The first volume of Immanuel Wallerstein's influential four-book The Modern World-System came out in 1974,

and the second in 1980. Wallerstein argued that the emergence of a

world-economy in which a specialization between manufacturing countries

in a "core" region and primary product exporters in a global "periphery"

helped to spur industrialization in the former and an unequal pattern

of development. He also linked the accretion of wealth in the periphery

to capital accumulation in the core, in line with the Williams debates

of the preceding decade. Indeed, Wallerstein cites Williams in volumes I

and III. In one sense, what Wallerstein and other writers with dependista

leanings, like Amin and Gunder Frank, did was to extend the Williams

thesis to apply to the broader process of unequal exchange with regions

outside the Western European core.

Wallerstein's books drew a heated response from Patrick O'Brien (1982)

in the EHR. O'Brien, in one of economic history's most memorable lines,

declared that "for the economic growth of the core, the periphery was

peripheral." Most of Europe's trade was internal and most of its

industries did not require large shipments of raw material. The

periphery generated only sufficient funds to finance 15 percent of

investment spending during the Industrial Revolution. And O'Brien

scoffed at the notion that "without imported sugar, coffee, tea,

tobacco, and cotton, [Western Europe's] industrial output could have

fallen by a large percentage." Leaving aside the empirically dubious

claim that the IR could really have functioned without cotton supplies,

O'Brien's figures don't really show that the periphery was very

peripheral. On the contrary, O'Brien estimates that for 1784–86, profits

from trade with the periphery amounted to £5.66 million, versus £10.30

million for Britain's total gross investment in the British economy—over

50%. Whether 7 percent is big or small may be debatable; 50 percent

isn't. Nevertheless, Wallerstein appears to have backed down in his

rather feeble 1983 comment on O'Brien's paper, in which he calls the claim that peripheral profits were essential to the IR a straw man.

A

number of studies tried to explicate the role of mercantile capital in

British, especially Scottish, industrialization. Devine (1976, 1977)

showed that profits from the Atlantic trade were invested in

shipbuilding, snuff mills, sugar refineries, glassworks, ironworks,

textiles, coal mines and other industries in London, the western ports,

and their hinterlands. Bristol, for example, had twenty sugar refineries

in its city center during the mid-eighteenth century and also housed

copper and brass works. Liverpool developed similar facilities. Glasgow,

home to the "tobacco lords," saw the rise of textiles, iron, sugar

refining, glassworks, and leather manufactories. Yet it's not possible

to show that the capital invested in these enterprises specifically came

from the peripheral trade, as opposed to the other domestic ventures in

which merchants engaged. Indeed, Devine (1975)

actually calculated that only 17 percent of the investment in

Scotland's cotton industry c. 1795 was financed by colonial traders; the

proportion financed by colonial funds must have

been even smaller. Further, Kindleberger (1975) argued that merchants

engaged in reselling products made small profits.

Wallerstein's

emphasis on the broader international pattern of trade, however,

offered a way past the old "small ratios" debates. Research during the

1980s began increasingly to focus on trade and manufacturing development

rather than investment funds, especially in light of the low levels of

fixed capital actually needed in most British enterprises. Inikori

(1987), for example, wrote that "To understand the broader relationships

[between slavery and industrialization] the emphasis must be shifted

from profits and the availability of investible funds to long-term

fundamental changes in England: the development of the division of labor

and the growth of the home market; institutional transformation

affecting economic and social structures, national values, and the

direction of state policy; and the emergence of development centers."

A special 1987 issue

of the Journal of Interdisciplinary History, later published as a

Solow-edited book (on the “legacy of Eric Williams”), heralded the

change in direction. Solow, Inikori, and even Richardson, the main

authors tackling the "industrialization" side, all accorded the Atlantic

economy an important role in British economic development. Solow's

article placed British slavery in the West Indies in the broader context

of European conquest-driven plantation agriculture and discussed the

formation, by 1700, of an "Atlantic system" (echoes of Wallerstein)

based on slavery. Britain shipped manufactures to North and Latin

America, Africa, and the West Indies. Africa exported slaves. The West

Indies bought slaves and manufactures while exporting sugar. Even the

free North American colonies were dependent indirectly on slave labor,

since they sold their timber and fish to the West Indies planters, using

the proceeds to buy British cottons and metal wares.

Solow

argued that "slave-sugar complex" increased economic activity in the

Atlantic basin, raising Britain's overall output thanks to the country's

(assumed) endemic underemployment, and boosting the productivity of

capital (investment) by introducing an elastic supply of labor. She also

drew a straight line between industrial exports (60 percent of

additional output over 1780-1800) and structural transformation. She

appears to back off the claim that slavery "caused" the Industrial

Revolution, but doesn't really, echoing Deane and Cole's argument that

exports drove the eighteenth-century surge in manufacturing and that the

American market took most of it. Solow's argument lacks, well, really

any kind of provable claim or supporting statistical foundation—of

course slavery was important, but by how much

against what counterfactual?—so it's hard to evaluate. But its general

drift exemplifies the new, expanded interpretation of the Williams

thesis as referring to the role of the entire Atlantic trading zone

existing solely because of coerced African labor.

Richardson

took a slightly different tack. Though his contemporary work on the

"numbers game" attacked the Inikori-Darity-Solow position on high

profits, he remained convinced that the slave-sugar complex contributed

to British industrialization (which makes his vitriol toward the trio

somewhat perplexing). His article points to the growth of British sugar

imports, tied to rising incomes partly, changing tastes, and the

availability of complementary goods (tea), in raising demand for British

exports in the Caribbean. African and American markets took 10 percent

of British exports in 1700 and 40 percent in 1800.

The

most important single factor [in driving the British export boom],

however, was rising Caribbean purchasing power stemming from mounting

sugar sales to Britain. As receipts from these sales rose, West Indian

purchases of labor, provisions, packing and building materials, and

consumer goods generally increased substantially after 1748, reinforcing

and stimulating in the process trading connections be-tween various

sectors of the nascent Atlantic economy. Data on changes in West Indian

incomes and expenditure at this time are unfortunately lacking, but …

gross receipts from British West Indian sugar exports to Britain rose

from just under £1.5 million annually between 1746 and 1750 to nearly

£3.25 annually between 1771 and 1775 or by about 117 percent.

Rising

West Indian proceeds from sugar sales had a direct impact on exports

from Britain to the Caribbean and, as planters expanded their purchases

of slaves from British slave traders, on exports from Britain to Africa

also. Customs records reveal that the official value of average annual

exports from Britain to the West Indies rose from £732,000 between 1746

and 1750 to £1,353,000 between 1771 and 1775, and that exports to Africa

rose over the same period from £180,000 to £775,000 per annum.

Like

Solow, Richardson also argues that North America's balance-of-payments

surplus with the Caribbean was necessary to offset its trade deficit

with Britain. Summing up, he finds that the West Indies added nearly

£1.75 million to British exports from the late 1740s to the early 1770s,

accounting for nearly 35 percent of the growth in British overseas

sales. But there's a twist. After accounting for re-exports, Richardson

finds that the Caribbean exports (of which 95 percent were manufactured)

accounted for just 12 percent of the growth (Deane & Cole numbers)

in British industrial output from 1748 to 1776. That's not nothing, but

it's hardly the stuff of revolutions, either. And it assumes that

resources used in producing Caribbean exports could not have been

reemployed, exaggerating the colonial contribution.

But Joseph

Inikori's article—"Slavery and the Development of Industrial Capitalism

in England"—is by the far the most sweeping. Borrowing from

development/trade economics and Marxist theory, Inikori adumbrates his

own theory of Britain's rise. Medieval England was a classic undeveloped

economy, lacking adequate markets for land, labor, and capital, with

little division of labor and bad institutions. Two autonomous forces

operate to produce economic and institutional change: population and

external commodity trade. Without the latter, the former tends to

produce Malthusian crises. Trade, however, lead to the development of

private property, the format of a landless proletariat, institutional

change, and the creation of a "sociological milieu" for scientific and

technological discovery. In short, basically all factors in British

development are endogenized to the growth of the export sector.

In

medieval England, the raw wool trade led to the cultivation of marginal

soils and the development of a land market, giving the country a more

"capitalist" internal structure than France. This allowed the English to

better exploit the opening of the Atlantic trade. As population growth

threw Continental economies into crisis, Britain tapped woolen markets

in southern Europe and for "other manufactures" in the Americas to

create employment opportunities outside agriculture. Inikori argues that

this foreign demand far exceeded that generated by income and

population growth at home. Indeed, both of the latter two were

consequences of trade (following Wrigley's early links between

demography and income)!

And trade was a consequence of slavery.

The New World's low populations and large natural resource base combined

with a high price of white labor raised slave prices in West Africa,

leading to the extension of coerced labor. Slaves were the workforce of

the American plantation economies, which in turn grew rapidly after the

late seventeenth century and furnished the exogenous demand for British

manufactures that drove institutional and structural change. Without

slaves, the "Atlantic system" would have been smalle. Without the

Atlantic system, the scaling up of textiles would have been impossible,

especially given the weakness of European demand for manufactures amid

Continental protectionism and proto-industrial development.

Inikori's

theory was the most complete and sophisticated to date in 1987—indeed,

it's more plausible than the one that Williams offered. The profits of

the slave trade are incidental to Inikori's narrative, being the

mechanism by which coerced labor was elastically supplied to New World

plantations. Nevertheless, the "Britain-as-East Asian-developing

country" story is incomplete. Why, for example, did Britain export sheep

in the Middle Ages, and why was the English state so enthusiastic about

and successful in doing so? Why didn't these agricultural commodity

exports prove a resource curse?

Inikori also doesn't really

explain the links between textile production and technological change,

and his assumption that discovery depends on "social context" is totally

half-baked. Same goes for institutions. It's actually sort of a

Smithian doux commerce take on North: institutions

and markets solve all problems, so we just need to explain why they

arise—and we can do it with the Atlantic trade! His explanation of why

Britain's colonies mattered, but those of her mercantile rivals didn't,

isn't an explanation at all—idiosyncrasies of colonies lead to

idiosyncratic national outcomes? Really? And treating export demand as

an exogenous factor discounts the role of internal factors (plantations

only exist because Englishmen want sugar), culture, and political

economy in creating export markets. Inikori also doesn't rigorously

explore backward linkages from wool to cotton (I guess textiles are

textiles!), obscures specifics of production technology, and ignores

coal, iron, and steam.

Nevertheless, the fact that Solow

and Engerman (who’d smited the Williams thesis fifteen years before) had

come together to edit the volume indicates a rough consensus about the

big thematic shift in how historians thought about the economics of the

slave trade. For the most part, they abandoned a very wrong position and

moved on to one that, despite less direct empirical evidence, is more

in line with our intuitions about how economic growth happens. We’ll

tackle that in Part II."

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.