Evaluating the free market by comparing it to the alternatives (We don't need more regulations, We don't need more price controls, No Socialism in the courtroom, Hey, White House, leave us all alone)

Saturday, May 12, 2018

Government Policy Mistakes Led to the Great Recession

By Peter Ireland and Darko Oračić. Peter Ireland is a Professor of Economics at Boston College and a

member of the Shadow Open Market Committee. Darko Oračić is an economic

analyst at the Croatian Employment Service.

"Most analysts agree that a housing boom and bust were the main

precipitating factor behind the deep economic crisis, now known as the

Great Recession, which took place a decade ago. And while there is no

universal consensus on what caused the housing boom and bust, these

events have, understandably, sparked many economists’ interest in

theories that financial market imperfections allow for excessive

volatility in asset prices that then lead to major fluctuations in

aggregate output and employment. Like older Keynesian theories, these

new models typically suggest that government policy intervention is

needed to curb risk-taking in financial markets and, more generally, to

counteract swings in consumer and business sentiment.

A few other economists, however, have described channels through

which government policies themselves may have created, or at least

amplified, the large fluctuations in home construction and prices that

preceded the Great Recession. These alternative theories suggest

instead that price movements generally operate, within a free market

system, to stabilize the economy when it is hit by disturbances to

aggregate supply and demand. Large disruptions to economic activity

occur only when policy mistakes work against the price system,

transforming what would otherwise be mild cyclical fluctuations into

more extreme booms and crashes. Here, we outline some arguments and

evidence to support this view, that the Great Recession was not the

inevitable consequence of unstable asset markets but followed, instead,

from a series of unfortunate government policy mistakes.

In a 2007 paper

presented at the Kansas City Fed’s Jackson Hole Symposium, John Taylor

of Stanford University presented evidence of a strong statistical

connection between data on housing starts and the federal funds rate

over the decade leading up to the crisis. Because the federal funds

rate is the interest rate under the most direct control of the Federal

Reserve, this correlation points to monetary policy as a potentially

destabilizing force during the boom-bust episode.

Some economists question this interpretation of the data, arguing

that the short-term interest rates under the Fed’s control have little

connection to the longer-term mortgages that finance the purchase of new

homes. A 2010 New York Fed working paper,

however, explains that banks and other mortgage providers borrow funds

on a short-term basis to make longer-term loans. Their activities open a

channel through which policy-induced movements in short-term rates

strongly affect the profitability of lending and thereby affect the

mortgage and housing markets.

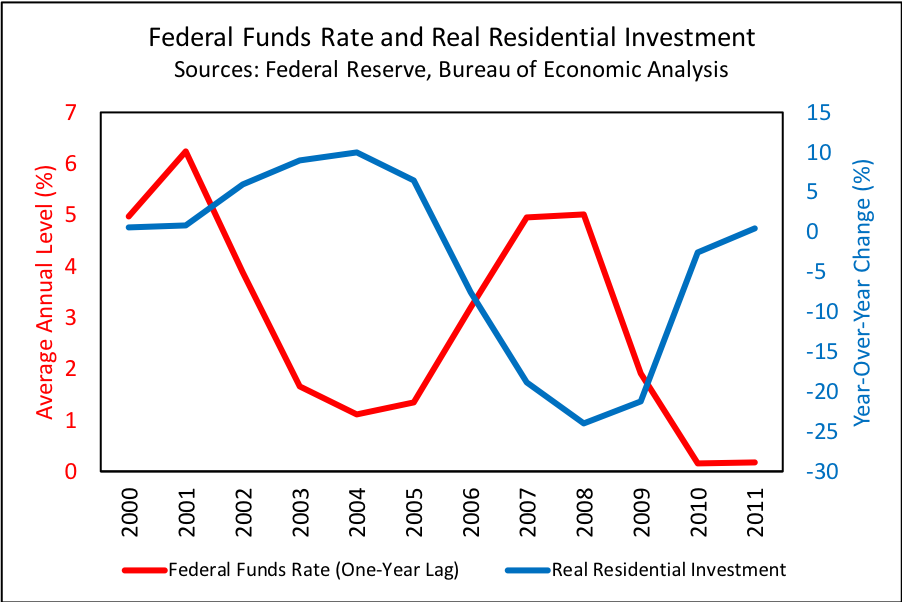

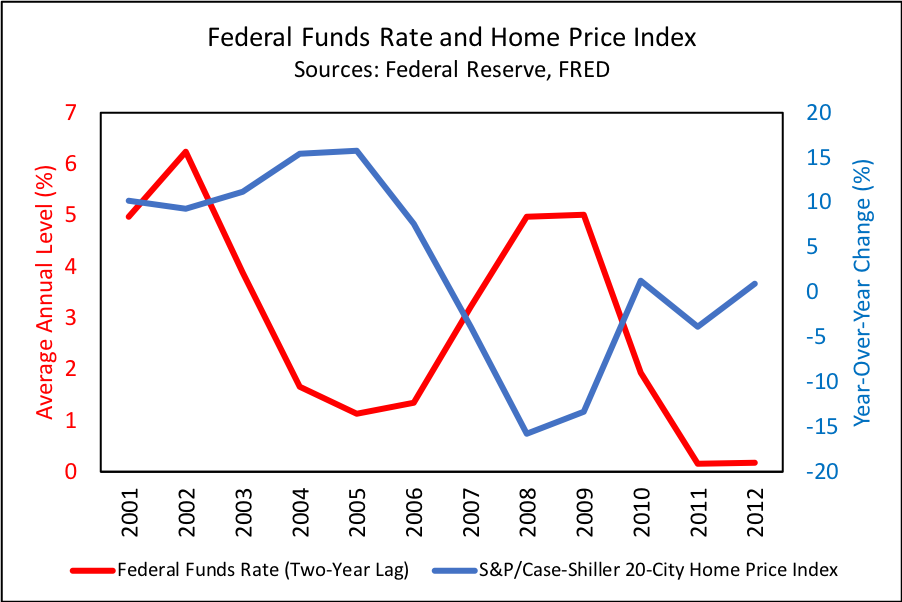

Other statistical indicators of housing-sector activity display

strikingly strong correlations with the federal funds rate. The first

figure below shows that rapid growth in residential investment over the

period from 2003 through 2005 was preceded by very low settings for the

federal funds rate. Then, a sharp decline in residential investment in

2007 and 2008 followed a period of higher federal funds rates. The

second figure displays a similar inverse correlation between lagged

values of the federal funds rate and subsequent changes in the

Case-Shiller home price index. These correlations are consistent with traditional accounts of the

manner and timing with which monetary policy disturbances affect

economic activity. Unusually accommodative policy leads, first, to an

“overheated” economy, as artificially low interest rates encourage

excessive spending on durable goods and, later, to higher rates of price

inflation. Conversely, overly-tight policy that keeps interest rates

too high works initially to choke off capital spending and subsequently

to lower inflation.

Of course, other forces were also at work during the housing cycle of 2003 through 2008. A very recent article

on the government sponsored agencies argues that federal subsidies to

mortgage borrowing and lending, offered through the now-bankrupt Fannie

Mae and Freddie Mac, introduced volatility and fragility into the U.S.

housing market before the crisis. Nevertheless, the correlations shown

in the graphs suggest that a prolonged episode of monetary policy that

was at first too accommodative and then too tight at least contributed

to and may even have been one of the principal causes behind the housing

boom and bust that led to the Great Recession.

Future research by economists, historians, and political scientists

will undoubtedly sharpen – and may even change – our view of what caused

the Great Recession. At present, however, our best bet is that the

crisis was not the inevitable consequence of inherent instability in US

asset markets. Rather, both the recession and housing crisis that

preceded it appear to have been the unintended consequences of

government policies that interfered with the workings of the price

system and destabilized what would otherwise have been much more

efficient markets."

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.