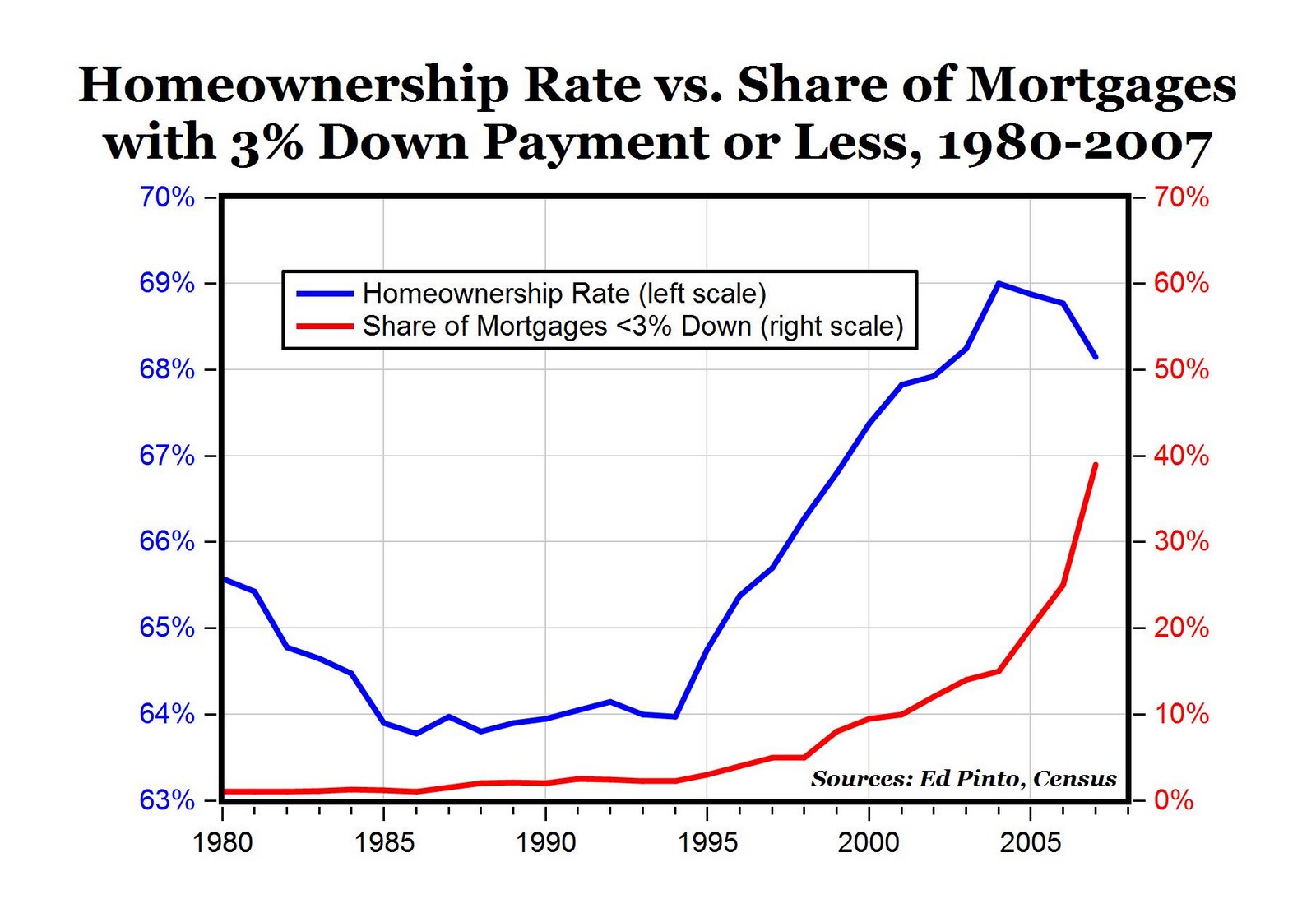

See

Britain's economic suicide by Matt Ridley.

"British Gas is putting up the cost of heating and lighting the average home by up to 18 per cent, or about £200 a year. Indignation at its profiteering is understandable. But that can only be a part of the story: the combined

profits of the big six energy supply companies amount to less than 1.5 per cent of your energy bill, according to the regulator, Ofgem.

Gas prices have gone up this year mainly because of demand from post-Fukushima Japan and booming China. With energy now a big part of household bills, genuine fuel poverty threatens many Britons next winter.

So what does the Government plan to do? This week it publishes a white paper on electricity market reform that will be predicated upon, indeed proud of, pushing up prices even faster. To meet its self-imposed green targets,

the Government’s policy is to tax carbon, fix high prices for renewable electricity and load extra costs on to people’s electricity bills — but without showing them as separate items.

This policy is beyond foolish. While you might just get away with driving up energy bills in a boom, to add green stealth taxes on top of supply-driven price increases at a time of economic misery is asking for political trouble.

Cheap energy is the elixir of economic growth. It was Newcastle’s cheap coal that gave the industrial revolution its second wind — substituting energy for labour drove up productivity, creating jobs and enriching both producers and consumers. Conversely, a dear-energy policy destroys jobs. Not only does it drive energy-intensive business overseas; according to Charles Hendry, the Energy Minister,

the average British medium-sized business will face an annual energy bill £247,000 higher by 2020 thanks to the carbon policy. That’s equivalent to almost ten jobs it must lose, or cannot create.

So the pain of this policy is huge. Yet even if it works,

the gain is tiny. The target is to get 15 per cent of total energy from renewables by 2020 — the current figure is just 1.8 per cent, not counting biomass and landfill gas. Most of that is old hydro; wind contributed less than half a per cent.

And that was the cheap bit.

The next generation of wind farms are going to be offshore and their electricity will cost three times as much. Even if we cover half the North Sea with wind farms, at gargantuan expense to the wretched consumer, and they manage to stay upright, we would still have to build gas turbines for when the wind fails to blow — as usually happens in exceptionally cold weather.

And, surprise, the energy companies are demanding subsidies for building gas-fired power stations that are to be unprofitably switched off when the wind blows.

Raising the costs of electricity to subsidise irrelevant wind farms will

fail to make the slightest dent in British carbon emissions, let alone global ones. In any case, natural gas is going to do far more than renewables ever could to accelerate the decarbonisation of the world economy, as it replaces high- carbon coal and oil in coming decades.

So the hijacking of energy policy by carbon targets is mad. Far more urgent questions face us than that. How do we replace the one-third of coal-fired stations that will close by 2015? Not by renewables, that’s for sure. How do we replace the capacity of our nuclear power stations, all but one of which will close by 2023? How do we compete with China, where it takes five years, not 15, to build a nuclear power station? How do we compete with America, where companies are now swimming in cheap domestic natural gas, half the price it is over here, thanks to shale gas exploration?

Gas already dominates the British energy market, providing about half of all joules. That dominance will only grow as abundant shale gas joins Russian and Iranian supplies. Given that renewables are an irrelevance in terms of supply, and that coal is being slowly phased out, the key question the Government needs to answer this week is where it wants to fix the price of nuclear electricity to ensure the long-term certainty nuclear investment requires.

Twenty years ago Britain liberalised its nationalised energy markets, introduced competition and the result was one of the cheapest and fairest regimes in the world. Gradually, the bureaucratic yearning to interfere and pursue ideology gained the upper hand again, especially with Tony Blair’s ludicrous “renewable obligation certificates” (ROCs) whose perverse consequences include the shipping of Californian native forest timber to Drax power station in Yorkshire at consumers’ expense.

This week’s White Paper is likely to suggest the replacement of these ROCs with a guaranteed price for renewable and nuclear power, partly reversible in the event that market prices exceed the guarantee. Unless very well designed, this too will have perverse consequences. In May alone National Grid paid wind farm users £2.6 million to switch their wind farms off.

Yet government has done very little to unleash energy entrepreneurs. We could have started the shale gas revolution here, as we started the fossil fuel revolution itself. We could still start the underground-coal gasification revolution here: according to a Newcastle firm called Five Quarter, huge amounts energy could be extracted from coal seams under the North Sea by partial combustion of the coal to make gas underground. We could push thorium reactors. But starting a business in Britain’s regulated economy and planning system is like swimming in treacle.

The future belongs to countries that can get their electricity, heat and fuel supplied as cheaply and reliably as possible. That is the priority, not the carbon fetish."

I defy you to look at that graph -- the green one -- and tell me that a temperature rise oif more than 2C is not "unlikely" according to that study. I defy you to look at the graph -- the blue one -- and not conclude that whoever drew it had better have a very good argument for fattening the tail compared with what the authors had originally published.

I defy you to look at that graph -- the green one -- and tell me that a temperature rise oif more than 2C is not "unlikely" according to that study. I defy you to look at the graph -- the blue one -- and not conclude that whoever drew it had better have a very good argument for fattening the tail compared with what the authors had originally published.

{kind=link}