"The Wall Street Journal reports on the details of the latest Keynesian binge.

Japan’s cabinet approved a government stimulus package that includes ¥7.5 trillion ($73 billion) in new spending, in the latest effort by Prime Minister Shinzo Abe to jump-start the nation’s sluggish economy. The spending program, which has a total value of ¥28 trillion over several years, represents…an attempt to breathe new life into the Japanese economy… The government will pump money into infrastructure projects… The government will provide cash handouts of ¥15,000, or about $147, each to 22 million low-income people… Other items in the package included interest-free loans for infrastructure projects…and new hotels for foreign tourists.As already noted, this is just the latest in a long line of failed stimulus schemes.

The WSJ story includes this chart showing what’s happened just since 2008.

And if you go back farther in time, you’ll see that the Japanese version of Groundhog Day has been playing since the early 1990s.

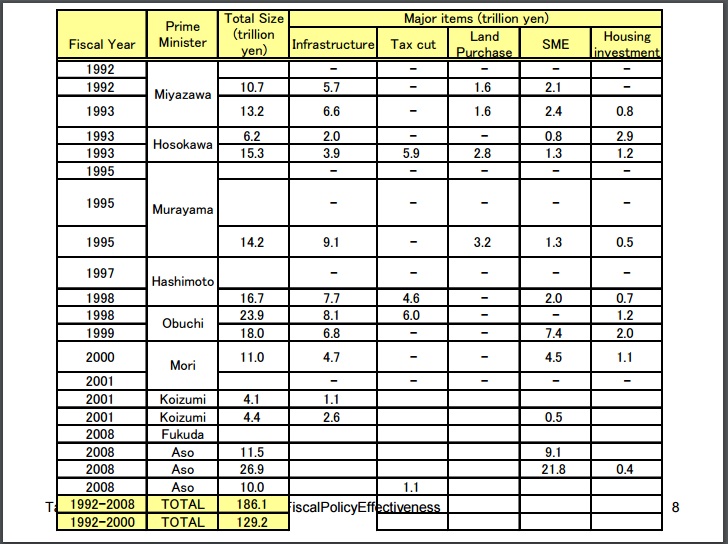

Here’s a list, taken from a presentation at the IMF, of so-called stimulus plans adopted by various Japanese governments between 1992-2008.

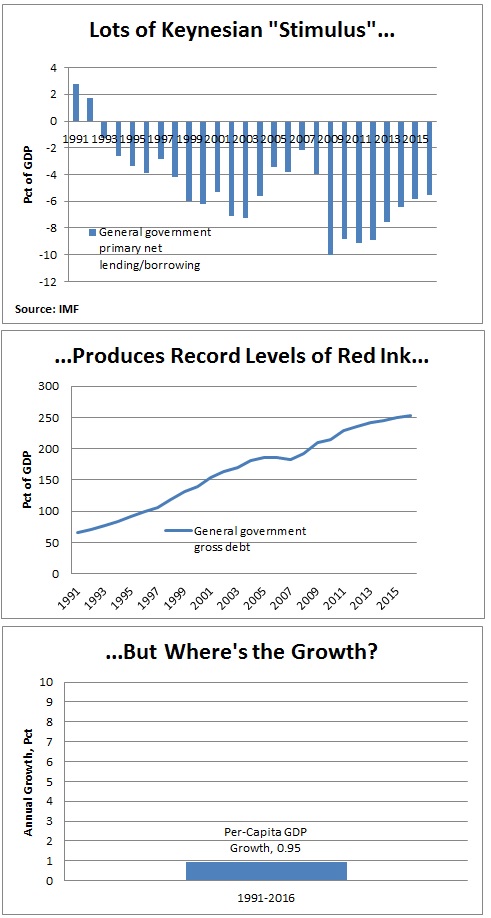

And here’s my contribution to the discussion. I went to the IMF’s World Economic Outlook database and downloaded the numbers on government borrowing, government debt, and per-capita GDP growth.

I wanted to see how much deficit spending there was and what the impact was on debt and the economy. As you can see, red ink skyrocketed while the private economy stagnated.

Though we shouldn’t be surprised. Keynesian economics didn’t work for Hoover and Roosevelt, or Bush and Obama, so why expect it to work in another country.

By the way, I can’t resist making a comment on this excerpt from a CNBC report on Japan’s new stimulus scheme.

Abe ordered his government last month to craft a stimulus plan to revive an economy dogged by weak consumption, despite three years of his “Abenomics” mix of extremely accommodative monetary policy, flexible spending and structural reform promises.In the interest of accuracy, the reporter should have replaced “despite” with “because of.”

In addition to lots of misguided Keynesian fiscal policy, there’s been a radical form of Keynesian monetary policy from the Bank of Japan.

Here are some passages from a very sobering Bloomberg report about the central bank’s burgeoning ownership of private companies.

Already a top-five owner of 81 companies in Japan’s Nikkei 225 Stock Average, the BOJ is on course to become the No. 1 shareholder in 55 of those firms by the end of next year…. BOJ Governor Haruhiko Kuroda almost doubled his annual ETF buying target last month, adding to an unprecedented campaign to revitalize Japan’s stagnant economy. …opponents say the central bank is artificially inflating equity valuations and undercutting efforts to make public companies more efficient. …the monetary authority’s outsized presence will make some shares harder to buy and sell, a phenomenon that led to convulsions in Japan’s government bond market this year. …the BOJ doesn’t acquire individual shares directly, it’s the ultimate buyer of stakes purchased through ETFs. …investors worry that BOJ purchases could give a free ride to poorly-run firms and crowd out shareholders who would otherwise push for better corporate governance.Wow. I don’t pretend to be an expert on monetary economics, but I can’t image that there will be a happy ending to this story."

Tuesday, August 16, 2016

Japan’s Slow-Motion Fiscal and Monetary Suicide

By Daniel J. Mitchell of Cato. Excerpt:

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.