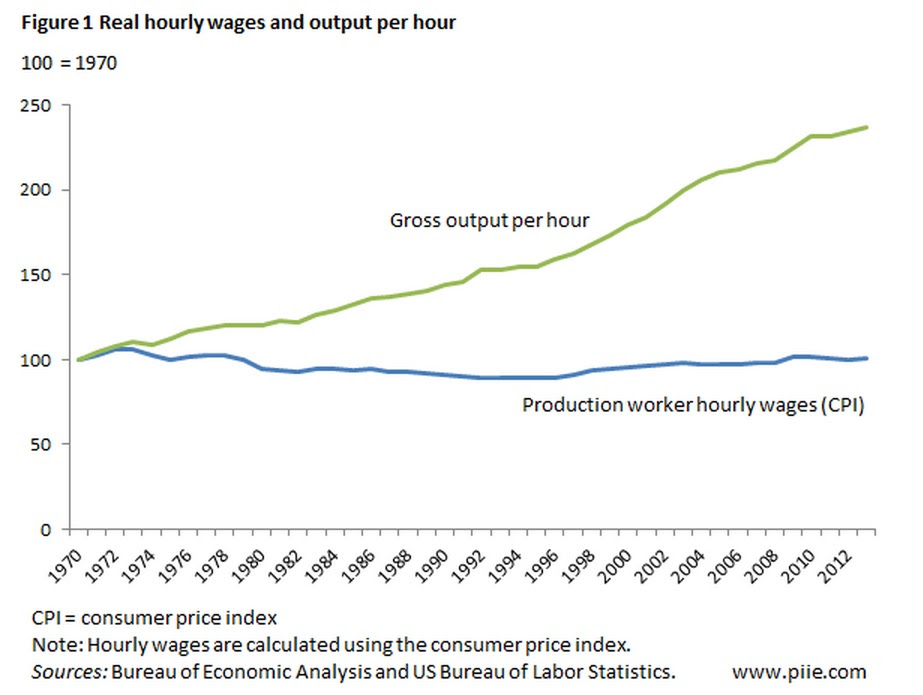

"Versions of the above [I moved it below-CM] chart are pretty common in news stories about inequality and middle class stagnation. While US output continues to rise decade after decade, the benefits don’t go to workers despite their obviously rising productivity. (And capital grabs more and more of national income.) There’s a big gap between the blue line (wages) and the green line (output).

But Robert Lawrence of the Peterson Institute argues this chart better reflects the productivity-worker income relationship:

According to this chart, wage and productivity growth have pretty much risen together. (And the share of national income going to labor has been steady until recently. More on that later.) Why the difference between the two charts? Lawrence made several modifications: (a) adjusted for an overly narrow definition of workers; (b) added in benefits to wages, (c) used an inflation measure that better accounts for what workers purchase; and (d) used a more relevant productivity measure. Lawrence:

Between 1970 and 2003 the growth in hourly real product compensation matched the growth in hourly real net output per worker. In 2003, therefore, the share of net compensation paid to labor was the same as in 1970. If the rise in average net output per hour is a good measure of the marginal product of labor, for this 33-year period, the data are compatible with the assumption that workers have actually seen their wages rise as rapidly as their marginal product. Since labor’s share in income fluctuates over the business cycle, and was therefore unusually high in 2000 for cyclical reasons, we cannot be confident about dating when the decline in labor’s share in income began. But it is clear that labor’s share has been unusually low since 2008, and real wages and compensation for workers of all skill levels has been slow.The explanation for the sluggish rise in real wages over the long run—1970 through 2000—may lie not with something that weakened labor’s bargaining power but instead in changes in the relative prices of the goods and services that workers consume and those that they produce. In particular, in thinking about policies to raise middle-class incomes, we should be concerned about (a) the rising relative prices of goods and services that workers consume such as housing and education; (b) the rising costs of benefits, especially health care, and (c) the slow productivity growth in services as compared with the rapid productivity growth in investment goods. In the period after 2000, the declining share of labor (and rising share of profits) does warrant further explanation (in a recent working paper, I argue this growing gap reflects a particular type of technical change), but prior to that, simplistic comparisons of “real” output per worker and “real” wages are likely to lead analysts to draw the wrong conclusions.This an uncomfortable analysis for analysts who argue that workers have been getting shafted for decades — and that the big reason why is the decline of union power. Instead, as I mentioned in the previous post, we need to focus first and foremost more on faster productivity and output growth. Then look at how these gains are being distributed."

Monday, July 27, 2015

Why the gap between worker pay and productivity might be a myth

From James Pethokoukis of AEI.

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.