"Prices for West Texas Intermediate crude oil -- often used as a benchmark of U.S. prices -- dropped below $70 per barrel for the first time since 2010. This continues a dramatic price slump for oil, which cost over $100 per barrel as recently as June."

"the Organization of the Petroleum Exporting Countries -- a group of 12 nations including Saudi Arabia, Iran and Venezuela that holds enormous power over global energy markets, producing 40 percent of global oil supply -- decided on Thursday not to cut production at their meeting in Vienna."

"Even as OPEC kept production steady, it has been growing elsewhere. The United States, most of all, has seen a major growth in oil production, thanks to the shale oil revolution, in which new technologies like horizontal drilling have allowed access to hydrocarbons deep beneath the Earth's surface.

The figures from the Energy Information Administration are truly dramatic: Almost twice as many barrels a day of crude oil are being produced now in the U.S., versus the mid-2000s:"

"Production of oil has also been up in many other countries."

" there's just more oil out there for people to buy, which is having a predictable effect on prices, pushing them downward."

"while the U.S. has recovered steadily from the Great Recession, many other countries have not. They're struggling, and that is dampening oil demand.

In Europe, for instance, while total petroleum consumption averaged over 15.3 million barrels per day in 2009, it was under 14.3 million in 2013, and has dropped further since."

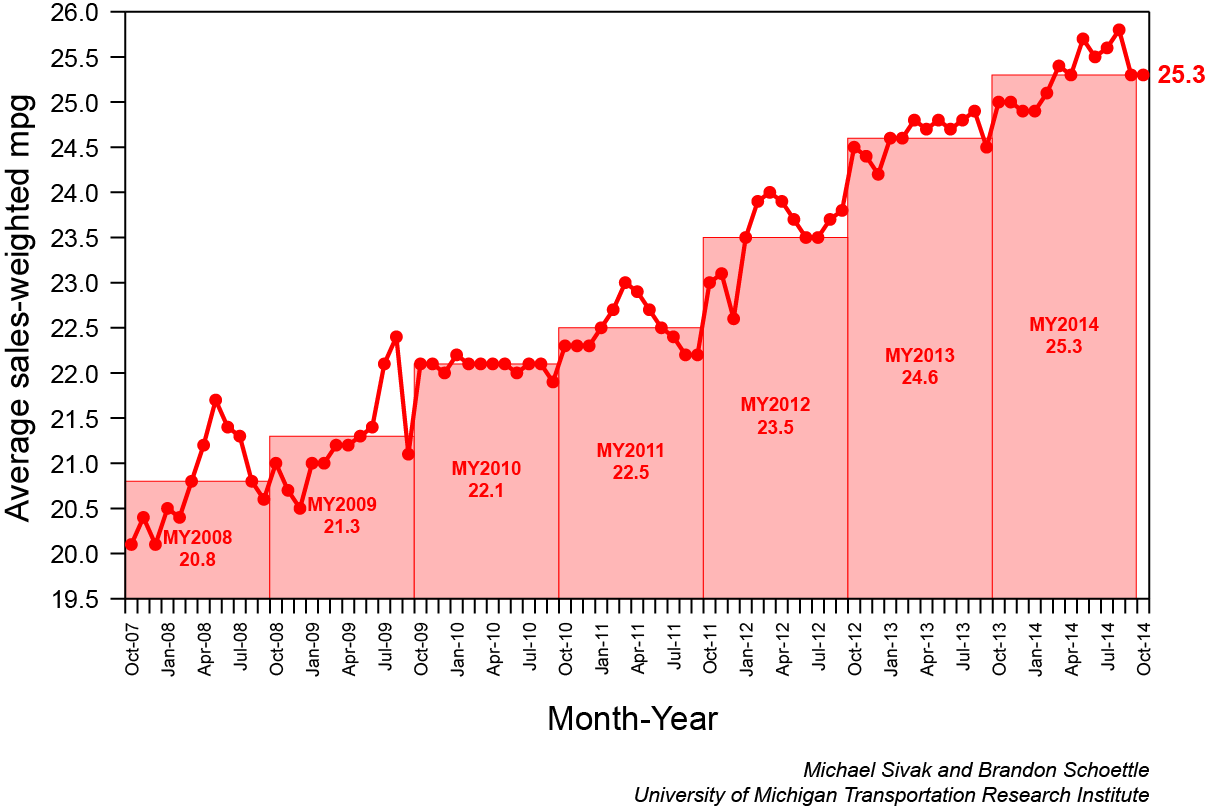

"In the U.S., we're also using less fuel in our cars because those cars are more efficient. The sales-weighted fuel economy of vehicles in the U.S. increased from 20.8 miles per gallon in 2008 to 25.3 miles per gallon in 2014."

Saturday, November 29, 2014

The trend in oil prices is due to that most basic of economic factors: Supply and demand

From Chris Mooney of the Washington Post. Excerpts:

{kind=link}

Subscribe to:

Post Comments (Atom)

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.